WHAT IS TAX CODE 1263L?

- Adil Akhtar

- Apr 11, 2024

- 19 min read

Updated: Jan 24

Understanding the UK Tax Code 1263L: A Comprehensive Guide

The UK tax code 1263L is a beacon for taxpayers, representing a specific threshold within the tax system that directly influences how much income tax you are liable to pay. This article delves into the essentials of the 1263L tax code, its implications for taxpayers, and guidance on managing changes to ensure compliance and optimise tax liabilities.

Deciphering Tax Code 1263L

The tax code 1263L signifies a personal allowance—the amount you can earn within a year without paying income tax—set at £12,630. This figure marks a slight increase from the commonly known 1257L tax code, which allows for a £12,570 tax-free personal income. The "L" in the tax code indicates that you're entitled to the standard personal allowance designated by Her Majesty's Revenue and Customs (HMRC).

The allocation of this tax code usually results from specific conditions or allowances recognised by HMRC, such as claims for work-related expenses. For instance, individuals may be assigned the 1263L code if they have successfully applied for allowances related to the maintenance of work uniforms, effectively increasing their personal allowance threshold.

Importance of the 1263L Tax Code for Taxpayers

For individuals at the brink of different tax brackets, the 1263L tax code could mean staying within a lower tax bracket, avoiding higher tax rates on a portion of their income. This nuanced aspect of the tax system underlines the importance of understanding your tax code, as it can significantly impact your overall tax bill.

Handling Changes in Your Tax Code

Tax codes are dynamic, often adjusted to reflect changes in income, employment status, or personal allowances. If you notice a shift in your tax code, it's vital to verify the change with HMRC, as inaccuracies can lead to underpayment or overpayment of taxes. Common triggers for tax code adjustments include variations in income, employment changes, alterations in benefits, and modifications to tax reliefs.

Steps for Updating Your Tax Code

Should you need to update your tax code, contacting HMRC is imperative. Providing accurate information regarding your annual income, company benefits, or any alterations in your pension is crucial for the recalibration of your tax code. HMRC will then issue a revised tax code, ensuring that your tax deductions accurately reflect your current financial situation.

The 1263L tax code plays a pivotal role in the UK tax system, offering a slightly elevated personal allowance and affecting a wide range of taxpayers. Understanding the implications of this tax code and maintaining open communication with HMRC to address any changes are fundamental steps in managing your tax obligations efficiently. Always check your tax code regularly and consult HMRC or a tax professional if you suspect discrepancies or need to update your tax-related information.

Tax Code 1263L: Navigating Adjustments and Implications

Understanding the intricacies of the UK tax code 1263L not only helps in ensuring you are taxed correctly but also unveils opportunities for potential tax savings. This part of our comprehensive guide sheds light on the mechanics behind tax code adjustments, the implications of having a 1263L code, and how it interfaces with the broader tax system.

The Mechanics of Tax Code Adjustments

Tax codes are tailored to individual financial circumstances, reflecting one's entitlement to personal allowances and any additional income or benefits. A change in your tax code can be prompted by various factors, such as alterations in your income, job transitions, adjustments in benefits, and variations in pension contributions. These modifications are pivotal as they ensure the tax code accurately mirrors your tax liability.

Key Considerations for Taxpayers with 1263L

The designation of the 1263L tax code to a taxpayer usually signifies an elevated personal allowance due to specific deductions or expenses, such as the uniform maintenance allowance. This increment in the tax-free allowance can subtly impact your net income, offering a buffer that could keep you within a lower tax bracket, thereby minimising your overall tax liability.

Responding to Changes in Your Tax Code

When confronted with a change in your tax code, it's crucial to undertake a verification process. Reviewing changes in your financial situation that might justify the new code is a good starting point. Should you find discrepancies or if the modification remains unexplained, contacting HMRC is a necessary step for clarification and correction.

The Role of HMRC in Tax Code Adjustments

The HMRC plays a central role in the determination and adjustment of tax codes. Keeping HMRC informed about significant changes in your income or employment status is essential for the accuracy of your tax code. Should you need to update your tax code, providing HMRC with comprehensive and up-to-date information will facilitate the correct calculation of your tax liabilities.

Proactive Tax Management Strategies

For individuals navigating the complexities of tax codes like 1263L, adopting a proactive approach towards tax management is advisable. This includes regularly checking your tax code, being vigilant about any changes in your financial circumstances, and understanding the implications of such changes on your tax code.

Leveraging Professional Advice

Given the dynamic nature of tax legislation and personal financial situations, consulting with tax professionals can provide clarity and strategic insights. This is particularly beneficial for individuals seeking to optimise their tax position, navigate complex tax issues, or understand the implications of specific tax codes on their financial health.

The tax code 1263L represents a segment of the UK tax system that, while seemingly straightforward, demands a nuanced understanding to leverage its benefits fully. Recognising the factors that can influence your tax code, understanding how to address changes, and taking advantage of professional advice are key components in managing your tax affairs efficiently. As tax codes continue to evolve, staying informed and proactive is paramount in ensuring that you are taxed fairly and are making the most of your income.

Mastering the 1263L Tax Code: Strategic Insights and Financial Planning

In this final segment of our guide, we delve into strategic financial planning and the broader implications of the 1263L tax code within the UK's tax framework. This exploration is designed to arm taxpayers with advanced insights for optimising tax liabilities and enhancing financial well-being.

Strategic Financial Planning with the 1263L Tax Code

The 1263L tax code, by elevating the personal allowance to £12,630, not only provides immediate financial relief but also opens avenues for strategic financial planning. This increased allowance can serve as a catalyst for taxpayers to re-evaluate their income sources, investment decisions, and tax-saving strategies to maximize their disposable income.

Utilising Allowances and Reliefs

A crucial aspect of tax planning involves understanding and utilising various allowances and reliefs available beyond the personal allowance. This includes savings allowances, dividend allowances, and potentially under-utilised reliefs such as marriage allowance or charitable giving reliefs. By comprehensively assessing these opportunities, taxpayers can further reduce their taxable income, leveraging the benefits of the 1263L tax code to its fullest potential.

Investment Strategies

The increased personal allowance under the 1263L code also influences investment strategies. Taxpayers might consider investing in ISAs or pensions, both of which offer tax-efficient growth. For higher-rate taxpayers on the cusp of different tax brackets, such investments can be particularly beneficial, potentially mitigating higher tax liabilities and optimising long-term financial outcomes.

Understanding the Implications of Additional Income

For those with multiple income streams, including self-employment or rental income, the 1263L tax code underscores the importance of meticulous financial management. Ensuring that all income is correctly declared and any allowable expenses are claimed can help in maintaining the tax efficiency afforded by the 1263L code.

Future-Proofing Your Tax Code

The dynamic nature of tax codes necessitates a proactive approach to tax affairs. Regularly reviewing your tax code, staying informed about legislative changes, and understanding how these affect your personal allowance and overall tax liability is crucial. For those whose financial circumstances change frequently, engaging with a tax professional can provide tailored advice and peace of mind.

Navigating Changes and Challenges

The UK tax system is ever-evolving, with annual adjustments to tax codes, allowances, and rates. Awareness and adaptability are key in navigating these changes effectively. Whether it's transitioning jobs, experiencing changes in income, or adjusting to new tax laws, understanding the implications on your tax code is fundamental to financial resilience and planning.

The 1263L tax code, while specific in its designation, plays a significant role within the broader tapestry of the UK tax system. It represents not just an increase in personal allowance but a prompt for individuals to engage more deeply with their tax affairs and financial planning. From leveraging allowances and reliefs to optimising investment strategies and navigating the complexities of additional incomes, the insights provided in this guide aim to equip taxpayers with the knowledge to make informed decisions.

Embracing a holistic approach to tax and financial planning can lead to significant benefits, ensuring that taxpayers not only comply with their obligations but also optimise their financial health. As we conclude this comprehensive exploration of the 1263L tax code, remember that staying informed, proactive, and engaged with your finances is the key to maximising your tax advantages and achieving your financial goals.

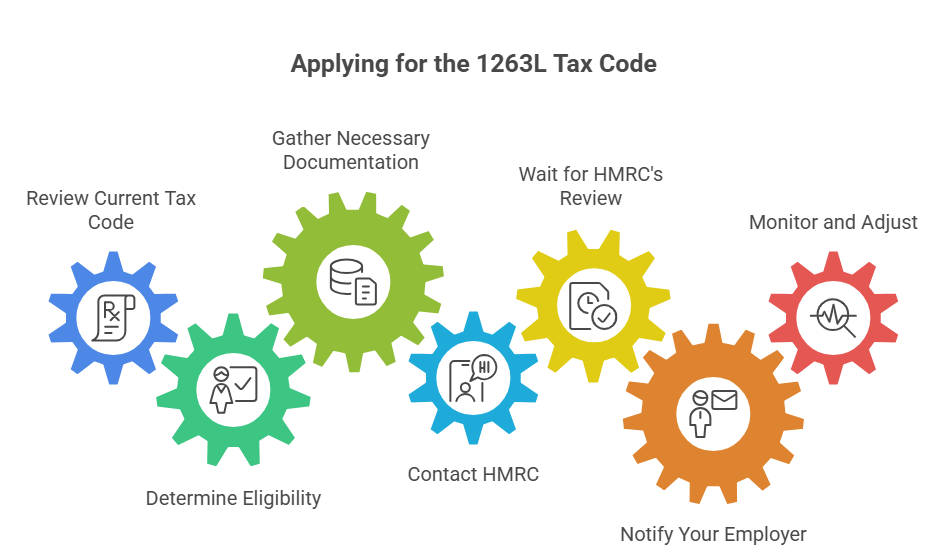

How to Apply for 1263L Tax Code - A Step By Step Guide

Applying for a specific tax code like the 1263L in the UK involves navigating the complexities of the tax system. This guide aims to simplify the process, ensuring you understand how to accurately secure the 1263L tax code, which could potentially offer you a slightly higher personal allowance, hence reducing your taxable income. Here's a step-by-step approach based on the general procedures of HM Revenue & Customs (HMRC) for tax code adjustments.

Understanding the 1263L Tax Code

Before applying for the 1263L tax code, it's crucial to grasp its implications. The 1263L tax code suggests a personal allowance of £12,630 for the tax year, allowing individuals to earn up to this amount before they are liable to pay income tax. This tax code is typically assigned to individuals who have certain allowances or deductions, such as uniform washing allowances, which effectively increase their tax-free income.

Step 1: Review Your Current Tax Code

Check Your Payslip: Your current tax code is listed on your payslip. Review it to confirm whether you're already on the 1263L code or another.

Access Your Personal Tax Account: HMRC provides an online service where you can view your tax code and historical tax codes for previous years.

Step 2: Determine Eligibility

Understand the Criteria: The 1263L tax code is generally assigned to those with specific deductions. Understanding these criteria is crucial to determining your eligibility.

Assess Your Allowances: If you believe you have untapped allowances, such as a uniform maintenance allowance, you might be eligible for the 1263L tax code.

Step 3: Gather Necessary Documentation

Proof of Expenses: Collect any receipts or documents that prove your eligibility for allowances or deductions influencing the 1263L code application.

Employment Details: Have your employment details ready, including your current tax code, PAYE reference number, and National Insurance number.

Step 4: Contact HMRC

Via Phone: HMRC's contact details are available on their official website. Calling them can be a direct approach to request a tax code change.

Online Form: For some allowances, such as the uniform washing allowance, you can apply directly through HMRC's website using specific forms like P87.

Writing: For those who prefer traditional methods, sending a detailed letter to HMRC with your request and supporting documentation is also an option.

Step 5: Wait for HMRC's Review

Processing Time: HMRC reviews applications and changes tax codes as needed. This process can take several weeks.

Notification: You will receive a notification from HMRC regarding the change to your tax code. This can be through your personal tax account or via post.

Step 6: Notify Your Employer

Share the Update: Once your tax code has been updated to 1263L, inform your employer. HMRC usually notifies them directly, but it’s good practice to ensure your payroll department is aware of the change.

Review Your Payslips: Check subsequent payslips to confirm the new tax code is being applied.

Step 7: Monitor and Adjust if Necessary

Keep Records: Maintain records of any allowances or deductions that justify the 1263L tax code.

Annual Review: Tax codes can change with new tax years or alterations in financial circumstances. Keep an eye on your tax code annually to ensure it remains accurate.

Tips for a Smooth Application Process

Be Proactive: Start the application process well before the end of the tax year to ensure any benefits from the tax code change can be realised as soon as possible.

Seek Advice: If you're unsure about your eligibility or the application process, seeking advice from a tax professional or HMRC can provide clarity.

Applying for the 1263L tax code is a process that requires a clear understanding of your eligibility, organised documentation, and proactive communication with HMRC. By following these steps, you can ensure that your tax code accurately reflects your financial circumstances, potentially reducing your tax liability. Always keep abreast of changes to tax legislation and your financial situation, as these could affect your tax code and overall tax obligations.

A Case Study of a UK Taxpayer Switching to 1263L Tax Code

This case study explores the journey of Alex, a UK-based professional, transitioning from the standard 1257L tax code to the 1263L code, highlighting the impact on their financial well-being and the procedural nuances involved in such a change. Through this scenario, we aim to encapsulate the comprehensive process, benefits, and considerations of switching tax codes within the UK tax system.

Background

Alex is a graphic designer employed full-time by a marketing firm in Bristol. For years, Alex has been on the standard 1257L tax code, which for the tax year 2025/2026, allows for a tax-free personal allowance of £12,570. However, after attending a financial wellness seminar, Alex learns about the 1263L tax code, which could offer a slightly higher personal allowance due to Alex's specific circumstances, potentially reducing their income tax liability.

Identifying Eligibility for the 1263L Tax Code

The first step in Alex's journey involves understanding the eligibility criteria for the 1263L tax code. This tax code signifies a personal allowance of £12,630 for the tax year, slightly higher than the standard allowance under the 1257L code. Alex discovers that eligibility for this tax code might include specific work-related expenses not reimbursed by the employer, such as professional subscriptions or uniform washing allowances.

Alex meticulously reviews their expenses and realizes they've been incurring professional subscription costs relevant to their role, which have not been reimbursed by their employer. Encouraged by this discovery, Alex decides to pursue a change in their tax code.

Consulting a Professional

Unsure how to proceed, Alex decides to consult a tax accountant, who confirms Alex's eligibility for the 1263L tax code based on their unreimbursed professional expenses. The accountant explains that transitioning to this tax code could indeed offer a slight reduction in Alex's taxable income, leading to modest annual savings on their income tax.

Applying for the Tax Code Change

Guided by their accountant, Alex gathers the necessary documentation, including evidence of the professional subscriptions, and submits a P87 form to HMRC for tax relief on these work-related expenses. The accountant assists Alex in accurately detailing the expenses and ensuring that the application highlights how these costs are integral to Alex's employment.

HMRC Review and Approval

After several weeks, HMRC reviews Alex's application and acknowledges the oversight in not accounting for these professional expenses in Alex's tax code. Subsequently, HMRC issues a new tax code notice to Alex, officially switching their code to 1263L for the current tax year. This adjustment reflects an increased personal allowance, accounting for the professional subscription expenses.

Impact on Financial Well-being

With the new 1263L tax code, Alex notices an immediate difference in their monthly take-home pay. Although the increase is modest, it represents a tangible benefit of being proactive about tax affairs. Over the year, the savings accumulate, offering Alex additional financial flexibility. This change also instills a greater sense of awareness in Alex about the nuances of the UK tax system and the importance of regularly reviewing one's tax code.

Reflections and Future Considerations

The transition to the 1263L tax code serves as a valuable financial lesson for Alex, highlighting the importance of understanding tax codes, recognising eligible expenses, and the benefits of consulting tax professionals. Going forward, Alex plans to keep meticulous records of potential work-related expenses and stay informed about changes in tax legislation that might affect their tax code or overall tax strategy.

Alex's journey from the 1257L to the 1263L tax code illustrates the procedural steps involved in changing tax codes in the UK, the potential financial benefits of such a transition, and the importance of understanding one's eligibility. This case study underscores the value of being proactive about tax affairs, the benefits of professional guidance, and the impact of tax codes on individual financial health within the UK's tax framework.

Through this hypothetical exploration, we aim to provide insight into the practical aspects of managing tax codes and encourage a proactive approach towards personal tax management. Alex’s story is a testament to the notion that with the right knowledge and resources, individuals can navigate the complexities of the tax system to their advantage.

How Can A Tax Accountant Help You With Your Tax Codes

Navigating the complexities of tax codes in the UK can be a daunting task for both individuals and businesses. The role of a tax accountant becomes invaluable in this landscape, providing clarity, ensuring compliance, and optimising tax positions. This detailed exploration reveals how a tax accountant can assist with understanding, applying, and adjusting tax codes to benefit taxpayers.

Understanding the Intricacies of Tax Codes

Tax codes in the UK are not just a series of letters and numbers; they signify an individual's tax allowances, deductions, and liabilities. A tax accountant brings a wealth of knowledge in decoding these codes, ensuring that taxpayers understand their implications. They can explain the difference between various tax codes, such as the 1257L, which represents the standard tax-free personal allowance, and the 1263L, indicating a slightly higher allowance. This fundamental understanding is crucial for taxpayers to ensure they are not overpaying or underpaying their taxes.

Tailored Advice and Strategy

Every taxpayer's situation is unique, influenced by their income sources, allowances, deductions, and specific life circumstances. Tax accountants provide personalised advice, considering all these variables to recommend the most beneficial tax code. For individuals with multiple income streams, various investments, or those who are self-employed, the guidance of a tax accountant is indispensable. They can strategise to utilise tax codes effectively, potentially leading to significant savings.

Assistance with Tax Code Changes

Life events such as changing jobs, receiving a pension, or alterations in investment income can necessitate a change in tax code. A tax accountant can navigate the bureaucratic processes required to update your tax code with HMRC, ensuring that the changes reflect your current financial situation accurately. They handle the necessary paperwork and communicate with HMRC on your behalf, alleviating the administrative burden from the taxpayer.

Resolving Discrepancies and Disputes

Discrepancies in tax codes can sometimes lead to overpayment or underpayment of taxes. Tax accountants are skilled in identifying such errors and can liaise with HMRC to correct them. In cases of disputes, they represent their clients, providing necessary documentation and arguments to resolve issues in their favor. Their expertise can be crucial in reclaiming overpaid taxes or negotiating settlements for underpayments.

Proactive Tax Planning

Beyond addressing immediate tax code concerns, tax accountants play a pivotal role in proactive tax planning. They keep abreast of changes in tax legislation that could affect their clients and suggest timely adjustments to tax codes or financial strategies. This foresight can minimise future tax liabilities and capitalise on available tax-saving opportunities.

Education and Empowerment

By demystifying the complexities of tax codes and the UK tax system, tax accountants educate their clients, empowering them to make informed financial decisions. They can provide workshops, detailed reports, and regular updates on tax matters, enhancing their clients' understanding and confidence in managing their taxes.

Compliance and Peace of Mind

Perhaps one of the most significant benefits of engaging a tax accountant is the assurance of compliance with UK tax laws. With their expertise, taxpayers can avoid the pitfalls of non-compliance, including penalties and audits. Having a professional oversee tax affairs provides peace of mind, allowing individuals and businesses to focus on their core activities without worrying about tax-related issues.

The role of a tax accountant in managing tax codes in the UK is multifaceted, offering not just remedial solutions but also strategic advantages. From ensuring accurate application of tax codes to optimising tax positions and ensuring compliance, a tax accountant is a valuable ally in navigating the complexities of the tax system. Whether you're an individual taxpayer looking to understand your tax code better or a business seeking to optimise your tax strategy, the expertise of a tax accountant can provide clarity, save money, and ensure peace of mind.

FAQs

Q1: Can I request a change to the 1263L tax code if I believe my circumstances no longer warrant it?

A: Yes, you can request a change to your tax code, including the 1263L, by contacting HMRC directly. You will need to provide them with detailed information about your current financial situation, including any changes in your income or employment status.

Q2: How does the 1263L tax code affect my eligibility for other tax benefits and reliefs?

A: The 1263L tax code primarily impacts your personal allowance. However, eligibility for other tax benefits and reliefs, such as Marriage Allowance or Blind Person’s Allowance, depends on broader tax rules and your specific circumstances. It's advisable to consult HMRC or a tax professional for advice tailored to your situation.

Q3: Is the 1263L tax code automatically updated each tax year?

A: Tax codes, including the 1263L, may be reviewed and updated by HMRC at the start of each tax year to reflect changes in personal allowances and tax legislation. It’s important to check your tax code each year to ensure it accurately reflects your circumstances.

Q4: What happens if I mistakenly use the 1263L tax code when I am not eligible?

A: If you use the 1263L tax code without being eligible, you may end up underpaying or overpaying tax. HMRC regularly reviews tax codes and will correct any discrepancies. It’s crucial to inform HMRC if you believe your tax code is incorrect to avoid potential issues.

Q5: Can the 1263L tax code be applied to both employment and pension income?

A: Yes, the 1263L tax code can be applied to employment and pension income if HMRC determines it's the correct code for your circumstances. However, specific rules apply to how tax codes are allocated across multiple income sources.

Q6: If I have additional income sources, like rental or investment income, does the 1263L tax code affect how this income is taxed?

A: The 1263L tax code primarily affects your tax-free personal allowance for employment or pension income. Additional income sources like rental or investment income are taxed according to different rules and are not directly impacted by your main employment tax code.

Q7: How do I inform HMRC about changes that might affect my 1263L tax code?

A: You can inform HMRC about changes affecting your tax code through your personal tax account online or by contacting them directly via phone. It’s important to report changes such as a new job, change in income, or cessation of work-related expenses promptly.

Q8: Can non-residents benefit from the 1263L tax code?

A: Non-residents typically do not qualify for the personal allowance and, by extension, specific tax codes like 1263L, unless they meet certain criteria outlined by HMRC. It’s advisable to check the latest HMRC guidelines or consult a tax professional.

Q9: What should I do if I receive a notice from HMRC changing my tax code from 1263L to another code?

A: If HMRC changes your tax code from 1263L to another code, review the notice for explanations of the change. If you disagree or don’t understand the reasons, contact HMRC directly for clarification or to dispute the change.

Q10: How does marriage or entering into a civil partnership affect the 1263L tax code?

A: Entering into a marriage or civil partnership can affect your tax code if you’re eligible to transfer allowances, such as the Marriage Allowance. This might lead to a change from the 1263L tax code, depending on your combined incomes and tax positions.

Q11: Are there any specific forms or documents I need to submit to HMRC to apply for or update the 1263L tax code?

A: To apply for or update your tax code to 1263L, you might need to submit a P87 form for work-related expenses or provide other documentation related to changes in your income or tax status. HMRC will guide you on the specific requirements based on your situation.

Q12: Does receiving a bonus at work affect my 1263L tax code?

A: Receiving a bonus can affect your overall tax liability, but it may not directly change your 1263L tax code. However, if your income changes significantly, HMRC might review and adjust your tax code as necessary.

Q13: How do tax code changes, including the 1263L, get communicated to employers or pension providers?

A: HMRC communicates any tax code changes, including changes to or from the 1263L, directly to your employer or pension provider through the PAYE system (PAYE). This ensures that the correct tax code is used when calculating your tax deductions. Employers and pension providers then apply the updated tax code to your salary or pension payments accordingly.

Q14: If I work part-time, will I still be assigned the 1263L tax code?

A: Whether you work part-time or full-time, the assignment of the 1263L tax code depends on your income level and eligibility for the personal allowance and other tax reliefs. HMRC determines your tax code based on your total income and circumstances.

Q15: Can I have two different tax codes if I have two jobs?

A: Yes, it's common to have different tax codes for each job if you have multiple employments. One job will typically use your personal allowance under a code like 1263L, while the second job might have a different code, reflecting that the personal allowance is already being used elsewhere.

Q16: What actions should I take if I retire during the tax year with a 1263L tax code?

A: Upon retirement, inform HMRC about your change in employment status. Your tax code may need to be adjusted based on your pension income and any other income sources you have in retirement.

Q17: Are self-employed individuals affected by the 1263L tax code?

A: The 1263L tax code applies to individuals taxed under the PAYE system. Self-employed individuals are taxed differently, using self-assessment tax returns to report their income and expenses. However, the personal allowance amount indicated by the 1263L code is relevant to all taxpayers, including the self-employed, in calculating their overall tax liability.

Q18: If I move abroad but still work for a UK-based company, does the 1263L tax code apply to me?

A: Tax residency status, rather than employment location, typically determines your eligibility for UK tax codes. If you move abroad, your tax residency and liability to UK income tax may change, potentially affecting the applicability of the 1263L code. Consulting with a tax professional and informing HMRC of your change in residency status is advisable.

Q19: How can I verify that the 1263L tax code is correct for my situation?

A: To verify that the 1263L tax code is correct for you, compare your personal allowance and taxable income against the criteria set by HMRC for this tax code. You can also use the HMRC online services or contact them directly for assistance in verifying your tax code.

Q20: What are the implications of the 1263L tax code for higher rate taxpayers?

A: For higher rate taxpayers, the 1263L tax code increases the threshold at which higher rates of tax are applied, due to the elevated personal allowance. This could potentially result in paying a lower amount of tax if the increased personal allowance keeps part of your income within the basic rate band. However, the overall impact depends on your total income and tax situation.

About the Author:

Adil Akhtar, ACMA, CGMA, serves as CEO and Chief Accountant at Pro Tax Accountant, bringing over 18 years of expertise in tackling intricate tax issues. As a respected tax blog writer, Adil has spent more than three years delivering clear, practical advice to UK taxpayers. He also leads Advantax Accountants, combining technical expertise with a passion for simplifying complex financial concepts, establishing himself as a trusted voice in tax education.

Email: adilacma@icloud.com

Disclaimer:

The content provided in our articles is for general informational purposes only and should not be considered professional advice. Pro Tax Accountant strives to ensure the accuracy and timeliness of the information but makes no guarantees, express or implied, regarding its completeness, reliability, suitability, or availability. Any reliance on this information is at your own risk. Note that some data presented in charts or graphs may not be 100% accurate.

We encourage all readers to consult with a qualified professional before making any decisions based on the information provided. The tax and accounting rules in the UK are subject to change and can vary depending on individual circumstances. Therefore, PTA cannot be held liable for any errors, omissions, or inaccuracies published. The firm is not responsible for any losses, injuries, or damages arising from the display or use of this information.

.png)