Tax Advice on SDLT Implications for Additional Property Purchases in 2025-26

- Adil Akhtar

- Jul 20, 2025

- 13 min read

The Audio Summary of the Key Points of the Article:

Understanding SDLT for Additional Property Purchases in 2025-26

What is Stamp Duty Land Tax and Why Does It Matter for Additional Properties?

Now, if you’re eyeing a second home or a buy-to-let property in 2025, Stamp Duty Land Tax (SDLT) is likely to be a significant chunk of your upfront costs. SDLT is a tax levied by HM Revenue & Customs (HMRC) on property or land purchases in England and Northern Ireland, applied when the purchase price exceeds certain thresholds. For additional properties—think second homes, holiday lets, or investment properties—the rules get a bit spicier because of a 5% surcharge introduced in the Autumn Budget 2024, effective from 31 October 2024, and further changes kicking in from 1 April 2025. This surcharge applies to anyone owning more than one residential property worth £40,000 or more, making it a critical consideration for investors and business owners.

The tax is calculated on a tiered basis, meaning different portions of the property price are taxed at different rates. Unlike standard residential purchases, additional properties face higher rates, which can significantly impact your budget. For example, a £350,000 buy-to-let purchase in 2025 could cost you thousands more in SDLT than a main home purchase at the same price. Understanding these rules is essential to avoid unexpected bills and plan your investments wisely.

How Do SDLT Rates Work for Additional Properties in 2025-26?

Let’s break it down with some numbers. From 1 April 2025, the SDLT thresholds and rates for additional properties in England and Northern Ireland will shift due to the end of temporary reliefs introduced in September 2022. The nil-rate threshold, where no SDLT is payable, drops from £250,000 to £125,000, and an extra 2% band is added for properties between £125,001 and £250,000. Here’s how the rates look for additional properties (on top of the standard rates):

Table 1: SDLT Rates for Additional Properties (1 April 2025 onwards)

Property Price Band | Standard Rate | Additional Property Rate (5% Surcharge) |

£0 - £125,000 | 0% | 5% |

£125,001 - £250,000 | 2% | 7% |

£250,001 - £925,000 | 5% | 10% |

£925,001 - £1,500,000 | 10% | 15% |

Over £1,500,000 | 12% | 17% |

So, the question is: how does this translate to your wallet? Imagine you’re buying a £400,000 buy-to-let property in May 2025. Here’s the breakdown:

● £0 - £125,000: £125,000 × 5% = £6,250

● £125,001 - £250,000: £125,000 × 7% = £8,750

● £250,001 - £400,000: £150,000 × 10% = £15,000

● Total SDLT: £6,250 + £8,750 + £15,000 = £30,000

Compare this to a main residence purchase at the same price, which would incur £7,500 in SDLT (0% on the first £125,000, 2% on the next £125,000, and 5% on the remaining £150,000). That’s a £22,500 difference, showing how the surcharge stings.

Who Pays the Higher Rates for Additional Properties?

Be careful! The higher rates apply if you own another residential property worth £40,000 or more anywhere in the world at the end of the transaction day, haven’t sold your previous main home, and the new property isn’t replacing your main residence. This catches a lot of people out. For example, if you own a flat in London and buy a holiday home in Cornwall, you’ll pay the surcharge. It also applies to:

● Buy-to-let investors

● Second-home buyers

● Companies or non-natural persons purchasing residential properties (with an additional 17% rate for properties over £500,000 from 31 October 2024)

● Non-UK residents, who face an extra 2% surcharge on top of the 5% surcharge

Here’s a quick case study to make it real. Meet Priya, a Birmingham-based dentist who owns her family home and wants to buy a £300,000 rental property in 2025. She hasn’t sold her main home, so she’s hit with the additional property rates:

● £0 - £125,000: £125,000 × 5% = £6,250

● £125,001 - £250,000: £125,000 × 7% = £8,750

● £250,001 - £300,000: £50,000 × 10% = £5,000

● Total SDLT: £20,000

If Priya had sold her main home before buying, she might have qualified for standard rates, saving thousands. Timing and ownership status are everything.

What About Non-UK Residents and Companies?

Now, here’s where it gets a bit trickier. If you’re a non-UK resident (not present in the UK for at least 183 days before the purchase), you’ll pay an additional 2% surcharge on top of the 5% surcharge, effective from 1 April 2021. For a £500,000 property, this adds another £10,000 to your SDLT bill. Companies or non-natural persons (like trusts) face even steeper rates. From 31 October 2024, properties over £500,000 purchased by companies are taxed at a flat 17%, which jumps to 17% on the entire purchase price for high-value properties.

For instance, consider a UK company controlled by a non-UK resident buying a £700,000 rental property in 2025. The SDLT would be:

● Entire price: £700,000 × 17% = £119,000

This is a hefty jump from the £60,000 Priya would pay as an individual for a similar property, highlighting the punitive rates for corporate buyers.

Navigating SDLT Reliefs, Exemptions, and Strategic Planning for 2025-26

Can You Avoid or Reduce the SDLT Surcharge for Additional Properties?

Now, let’s get to the juicy part—ways to legally dodge or reduce that hefty 5% SDLT surcharge for additional properties in 2025-26. Nobody wants to pay more tax than necessary, right? The good news is that HMRC offers several reliefs and exemptions that can ease the burden, but they come with strict conditions. Knowing these can save you thousands, whether you’re a buy-to-let landlord or snapping up a holiday home. Let’s explore the key ones and how they apply.

First, there’s Multiple Dwellings Relief (MDR), which can be a game-changer if you’re buying more than one residential property in a single transaction, like a block of flats. MDR spreads the SDLT calculation across the average price of each dwelling, potentially lowering the overall tax. However, the Autumn Budget 2024 tightened MDR rules, reducing its generosity from 1 April 2025. For example, if you buy six flats for £1.2 million (£200,000 each), you’d calculate SDLT on the average price (£200,000) per dwelling, then multiply by six, often resulting in a lower bill than taxing the total £1.2 million.

Another option is main residence replacement. If you sell your main home and buy another within three years, you might reclaim the 5% surcharge paid on the new purchase. This is a lifesaver for those moving homes but temporarily owning two properties. Take Sanjay, a Leeds-based IT consultant, who buys a £450,000 new home in June 2025 while still owning his old £300,000 flat. He pays the surcharge (£33,500 total SDLT) but sells his flat within three years. He can claim a refund of £13,500 (the surcharge portion), bringing his SDLT to the standard rate.

Are There Exemptions for Specific Property Types?

Now, here’s something you might not know: not all properties trigger the higher SDLT rates. Mixed-use properties—those with both residential and commercial elements, like a shop with a flat above—fall under non-residential SDLT rates, which are lower and don’t carry the 5% surcharge. As of 1 April 2025, non-residential rates are:

Table 2: Non-Residential SDLT Rates (1 April 2025 onwards)

Property Price Band | Rate |

£0 - £150,000 | 0% |

£150,001 - £250,000 | 2% |

Over £250,000 | 5% |

Source: HMRC Non-Residential SDLT Rates

Imagine Ayesha, a Manchester-based entrepreneur, buying a £500,000 mixed-use property (a café with a flat) in 2025. Her SDLT calculation would be:

● £0 - £150,000: £150,000 × 0% = £0

● £150,001 - £250,000: £100,000 × 2% = £2,000

● £250,001 - £500,000: £250,000 × 5% = £12,500

● Total SDLT: £14,500

Compare this to a purely residential property at £500,000, which would cost £37,500 in SDLT with the surcharge. That’s a £23,000 saving! But be warned: HMRC scrutinises mixed-use claims, so the commercial element must be genuine.

Properties deemed uninhabitable at purchase—like derelict buildings requiring major renovation—may also qualify for non-residential rates. However, post-Budget 2024, HMRC tightened definitions, so seek professional advice before banking on this.

How Can Business Owners Strategically Plan SDLT Costs?

So, the question is: how can savvy business owners or investors minimise SDLT in 2025-26? Timing and structure are everything. Here are some practical strategies:

● Buy before threshold changes: The nil-rate threshold for additional properties drops from £250,000 to £125,000 on 1 April 2025. If you’re planning a purchase, completing before this date could save you thousands. For a £200,000 property, SDLT before 31 March 2025 is £5,000 (5% on £200,000); after, it’s £7,500 (5% on £125,000 + 7% on £75,000).

● Use a limited company: For high-value properties, buying through a company can trigger the flat 17% rate, which sounds steep but may simplify tax planning for corporate investors. However, weigh this against other taxes like Corporation Tax.

● Consider joint ownership: If you’re married or in a civil partnership, buying jointly with a spouse who doesn’t own property can avoid the surcharge, provided the property becomes your main residence.

● Claim MDR for bulk purchases: If you’re a developer or landlord buying multiple properties, MDR can still offer savings, even with 2024 restrictions. Always consult a tax advisor to ensure eligibility.

Here’s a case study to illustrate. Meet Tariq, a Bristol property developer, who plans to buy three rental flats for £750,000 in July 2025. Without MDR, his SDLT would be:

● £0 - £125,000: £125,000 × 5% = £6,250

● £125,001 - £250,000: £125,000 × 7% = £8,750

● £250,001 - £750,000: £500,000 × 10% = £50,000

● Total: £65,000

With MDR, he calculates SDLT on the average price (£250,000 per flat):

● Per flat: £125,000 × 5% + £125,000 × 7% = £15,000

● Total for three flats: £15,000 × 3 = £45,000

That’s a £20,000 saving, showing how MDR can make a difference.

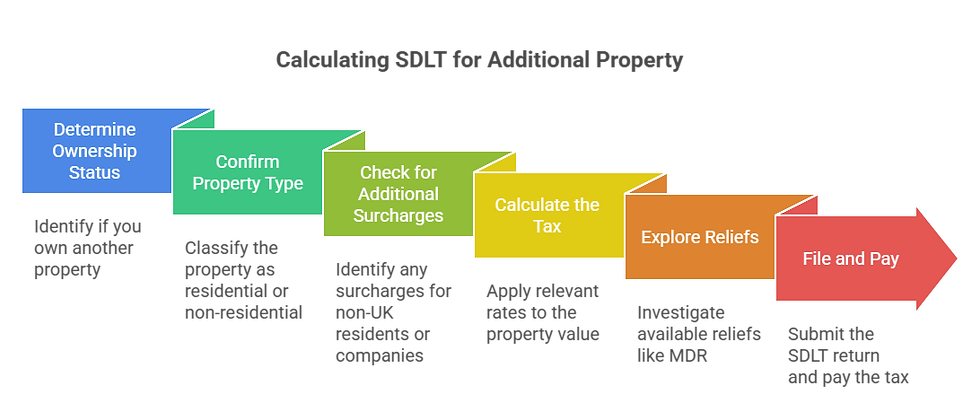

Step-by-Step Guide: Calculating SDLT for an Additional Property

None of us loves crunching numbers, but calculating SDLT accurately can save you from nasty surprises. Follow these steps for a 2025-26 purchase:

Determine ownership status: Check if you own another property worth £40,000 or more. If yes, the 5% surcharge applies.

Confirm property type: Is it residential, non-residential, or mixed-use? Use the appropriate rate table.

Check for additional surcharges: Non-UK residents add 2%; companies may face the 17% rate.

Calculate the tax: Break the purchase price into bands and apply the relevant rates (see Table 1 or 2).

Explore reliefs: Check eligibility for MDR, main residence replacement, or other exemptions.

File and pay: Submit your SDLT return and pay within 14 days of completion via HMRC’s online portal.

For example, if you’re buying a £350,000 buy-to-let as a UK resident, the steps above yield an SDLT of £24,500 (as calculated in Part 1). Use HMRC’s SDLT calculator for precision.

What Are the Risks of Getting SDLT Wrong?

Be careful! Misjudging SDLT can lead to penalties or missed reliefs. Common pitfalls include:

● Misclassifying properties: Claiming mixed-use status for a property that’s primarily residential can trigger HMRC audits.

● Missing deadlines: You must file and pay SDLT within 14 days of completion, or face fines starting at £100.

● Overlooking refunds: If you sell your main home within three years, claim the surcharge refund promptly via HMRC’s refund process.

A 2024 case study from HMRC’s records highlights this. A couple, Elowen and Jago from Cornwall, paid the 5% surcharge on a £400,000 second home in 2023. They sold their main home in 2024 but forgot to claim a refund within the three-year window, missing out on £12,000. Don’t let this be you—set reminders and consult a tax advisor for complex cases.

Key Takeaways on SDLT for Additional Property Purchases in 2025-26

Why Should You Care About SDLT Planning?

Now, if you’re still with me, you’ve likely got a good grasp of how Stamp Duty Land Tax (SDLT) can impact your plans to buy that second home or investment property in 2025-26. It’s not just about paying the tax—it’s about understanding how to navigate the rules to keep more money in your pocket. This final part pulls together the most critical points to ensure you’re armed with the knowledge to make smart decisions. Whether you’re a buy-to-let landlord or a business owner eyeing a property portfolio, these takeaways will help you avoid costly mistakes and maximise savings.

Below are the ten most important points to remember, distilled into clear, actionable insights. Each point is designed to guide you through the complexities of SDLT for additional properties, based on the latest rules effective from 1 April 2025 and updates from the Autumn Budget 2024.

Additional properties face a 5% SDLT surcharge. If you own another residential property worth £40,000 or more, you’ll pay an extra 5% on top of standard SDLT rates for purchases in England and Northern Ireland, as updated in the Autumn Budget 2024.

SDLT thresholds change from 1 April 2025. The nil-rate threshold for additional properties drops from £250,000 to £125,000, increasing tax liabilities for properties above this value, with a new 7% band for £125,001–£250,000.

Rates for additional properties are higher. For example, a £400,000 buy-to-let property incurs £30,000 in SDLT (5% on £125,000, 7% on £125,000, 10% on £150,000), compared to £7,500 for a main residence.

Non-UK residents pay an extra 2% surcharge. If you’re not UK-resident (present less than 183 days), you’ll face an additional 2% on top of the 5% surcharge, adding £10,000 to SDLT on a £500,000 property.

Companies face a flat 17% rate for high-value properties. From 31 October 2024, companies buying residential properties over £500,000 pay 17% SDLT on the entire price, making corporate purchases costlier.

Multiple Dwellings Relief (MDR) can save thousands. Buying multiple residential properties in one transaction (e.g., a block of flats) allows you to calculate SDLT on the average price per dwelling, potentially reducing the bill, though 2024 rules tightened eligibility.

Main residence replacement offers refunds. Sell your main home within three years of buying a new one, and you can reclaim the 5% surcharge, as seen in cases like Sanjay’s £13,500 refund on a £450,000 purchase.

Mixed-use properties dodge the surcharge. Properties with commercial and residential elements (e.g., a shop with a flat) use lower non-residential rates (0%–5%), saving significant amounts, like Ayesha’s £23,000 saving on a £500,000 property.

Strategic timing can reduce costs. Completing purchases before the 1 April 2025 threshold drop can save thousands, as a £200,000 property’s SDLT rises from £5,000 to £7,500 post-change.

Accurate filing avoids penalties. File your SDLT return and pay within 14 days of completion via HMRC’s portal to avoid fines starting at £100, and check eligibility for reliefs like MDR or refunds.

FAQs

Q1: What is the definition of an additional property for SDLT purposes?

A1: An additional property is any residential property purchased by an individual or entity who already owns another residential property worth £40,000 or more, anywhere in the world, and is not replacing their main residence.

Q2: How does the SDLT surcharge affect joint property purchases?

A2: If any joint purchaser owns another residential property, the 5% SDLT surcharge applies to the entire purchase, unless the property is a main residence replacement for all parties involved.

Q3: Can first-time buyers be exempt from the SDLT surcharge on additional properties?

A3: First-time buyers are not exempt from the 5% surcharge if they buy an additional property and already own another residential property worth £40,000 or more.

Q4: What happens if a property is purchased through a trust?

A4: Properties bought through a trust are subject to the 5% SDLT surcharge if the trust or beneficiary owns another residential property, and corporate trusts may face the 17% flat rate for properties over £500,000.

Q5: Is SDLT payable on inherited properties?

A5: Inherited properties do not incur SDLT as they are not purchases, but buying an additional property while owning an inherited one triggers the 5% surcharge.

Q6: Can the SDLT surcharge be avoided by transferring property ownership?

A6: Transferring ownership to a spouse or civil partner who doesn’t own property may avoid the surcharge if the property becomes their main residence, but HMRC scrutinises such arrangements for tax avoidance.

Q7: How does SDLT apply to properties bought for children or dependants?

A7: If a parent buys a property for a child and retains ownership, the 5% surcharge applies if the parent already owns another property, regardless of the child’s ownership status.

Q8: What are the SDLT implications for buying a leasehold property as an additional property?

A8: Leasehold properties are treated as residential properties, so the 5% surcharge applies if the buyer owns another property, with SDLT calculated on the lease premium and any rent.

Q9: Can SDLT be deferred or paid in instalments for additional property purchases?

A9: SDLT must be paid within 14 days of completion, and HMRC does not generally allow deferral or instalments, though financial hardship cases can be discussed with HMRC.

Q10: How does SDLT apply to properties purchased for commercial letting?

A10: Properties bought for commercial letting, like buy-to-lets, are subject to the 5% SDLT surcharge if the buyer owns another residential property, unless classified as non-residential.

Q11: What is the SDLT treatment for holiday lets?

A11: Holiday lets used for commercial purposes may qualify for non-residential SDLT rates, avoiding the 5% surcharge, but only if they meet strict HMRC criteria for commercial use.

Q12: Can SDLT be reclaimed if a property purchase falls through?

A12: If a property purchase is cancelled before completion, no SDLT is due, but if paid and the transaction fails, a refund can be claimed via HMRC’s process.

Q13: How does SDLT apply to properties bought in a divorce settlement?

A13: Properties transferred as part of a divorce settlement are exempt from SDLT, but purchasing an additional property during or after divorce triggers the 5% surcharge if the buyer owns another property.

Q14: What are the SDLT rules for buying a granny annexe as an additional property?

A14: A granny annexe bought as part of a main residence may qualify for Multiple Dwellings Relief, but if purchased separately and the buyer owns another property, the 5% surcharge applies.

Q15: Can SDLT be reduced for energy-efficient additional properties?

A15: There are no specific SDLT reliefs for energy-efficient properties, but mixed-use or non-residential classifications could lower the tax if applicable.

Q16: How does SDLT apply to off-plan property purchases?

A16: Off-plan properties are subject to the same SDLT rules, with the 5% surcharge applying if the buyer owns another property at completion, based on the final purchase price.

Q17: What are the penalties for late SDLT payment on additional properties?

A17: Late SDLT payment incurs a £100 fine if within 3 months, £200 if later, plus interest at 7.75% annually, with further penalties for late filing of returns.

Q18: Can SDLT be offset against other taxes for additional property purchases?

A18: SDLT cannot be offset against other taxes like Income Tax or Corporation Tax, as it is a separate transaction-based tax.

Q19: How does SDLT apply to properties bought at auction?

A19: Auction purchases follow the same SDLT rules, with the 5% surcharge applying if the buyer owns another property, and payment due within 14 days of completion.

Q20: What documentation is needed to claim an SDLT refund for main residence replacement?

A20: To claim a refund, submit an amended SDLT return with proof of the main residence sale, such as conveyancing documents, within three years of the original purchase.

About The Author:

Adil Akhtar, ACMA, CGMA, CEO and Chief Accountant of Pro Tax Accountant, is an esteemed tax blog writer with over 10 years of expertise in navigating complex tax matters. For more than three years, his insightful blogs have empowered UK taxpayers with clear, actionable advice. Leading Advantax Accountants as well, Adil blends technical prowess with a passion for demystifying finance, cementing his reputation as a trusted authority in tax education.

Email: adilacma@icloud.com

Disclaimer:

The information provided in our articles is for general informational purposes only and is not intended as professional advice. While we strive to keep the information up-to-date and correct, Pro Tax Accountant makes no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the website or the information, products, services, or related graphics contained in the articles for any purpose. Any reliance you place on such information is therefore strictly at your own risk. Some of the data in the above graphs may to give 100% accurate data.

We encourage all readers to consult with a qualified professional before making any decisions based on the information provided. The tax and accounting rules in the UK are subject to change and can vary depending on individual circumstances. Therefore, Pro Tax Accountant cannot be held liable for any errors, omissions, or inaccuracies published. The firm is not responsible for any losses, injuries, or damages arising from the display or use of this information.

.png)