Figuring Out Salary After Taxes

- Adil Akhtar

- May 3

- 20 min read

Figuring Out Your Salary After Taxes in 2026: A UK Taxpayer's Complete Guide

Understanding Take-Home Pay Beyond the Basics - Why Most Salary Calculators Miss the Mark

Picture this: you've just been offered a £45,000 position, and you immediately punch the figure into an online calculator. It spits out a number, and you think you're done. Here's where I've seen countless clients slip up over my 18 years advising UK taxpayers—those generic calculators rarely account for the nuances that genuinely affect your pocket.

Your actual take-home depends on factors most people overlook: your tax code anomalies, whether you're Scottish or based elsewhere in the UK, student loan deductions, pension contributions (and whether they're salary sacrifice or relief-at-source), benefits in kind that don't appear on your payslip, and crucially for 2025/26, how employer National Insurance changes might indirectly affect your package.

The 2025/26 Tax Landscape: What's Actually Changed

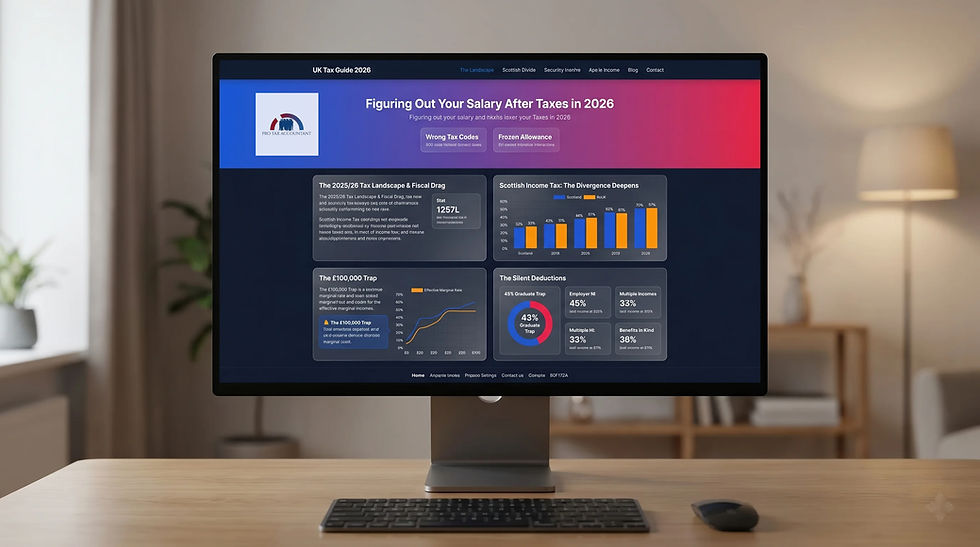

Let's be honest—none of us likes tax surprises, especially when thresholds remain frozen whilst inflation quietly erodes purchasing power. For 2025/26, the personal allowance stays at £12,570, exactly where it's been since April 2021. The basic rate threshold remains £50,270, and the additional rate kicks in at £125,140.

What many don't realise is this: with wage growth averaging around 5-6% annually but tax bands frozen until at least April 2028, you're experiencing fiscal drag. That promotion might push you into the 40% bracket when historically you'd have stayed at 20%. This isn't theoretical—the Office for Budget Responsibility estimates an additional 3.2 million taxpayers will be dragged into higher rates by 2028 purely through frozen thresholds.

The Tax Code Puzzle Most People Get Wrong - Decoding What Your Tax Code Actually Means

Now, imagine you're looking at your payslip and it says "1257L"—do you know what that means beyond "probably standard"? That L indicates you're entitled to the basic personal allowance. The numbers (1257) represent your tax-free amount: £12,570 with the final digit dropped.

Where clients frequently go wrong is assuming their code is correct. In my experience, roughly one in seven employed individuals has an incorrect tax code at some point during the year. This happens because HMRC makes assumptions based on previous year data, employer reporting lags, or benefits aren't properly coded.

Emergency Tax Codes: The Silent Pay Thief

Here's a scenario I see repeatedly: someone starts a new job mid-year without providing a P45. Their employer uses code 1257L W1/M1—an emergency code. This means you're taxed on a non-cumulative basis, potentially overpaying if you had months earlier in the year with no income.

Think of it like this: on a cumulative code, your tax is calculated from 6 April onwards, averaging your allowance across the whole year. On emergency tax, each pay period stands alone. You could legitimately be due a £2,000 refund but won't see it until you either provide your P45 or HMRC processes your records properly.

Scottish Income Tax: The Divergence Deepens - How Scottish Rates Fundamentally Differ

If you're earning £40,000 in Glasgow versus £40,000 in Cardiff, your take-home is materially different. Scotland now operates six income tax bands compared to England, Wales and Northern Ireland's three bands. For 2025/26, Scottish rates are: 19% starter rate (£12,571-£15,397), 20% basic rate (£15,398-£27,491), 21% intermediate rate (£27,492-£43,662), 42% higher rate (£43,663-£75,000), 45% advanced rate (£75,001-£125,140), and 48% top rate (above £125,140).

The crossover point—where Scottish taxpayers start paying more—is approximately £28,850. Below this, you're marginally better off in Scotland. Above it, particularly between £43,663 and £125,140 where you're paying 42-45% versus England's 40%, the difference compounds.

The Scottish Tax Code Identifier You Might Miss

Your tax code should start with 'S' if you're a Scottish taxpayer. This isn't about where your employer is located—it's about where you live. I've worked with clients who moved from Manchester to Edinburgh mid-year but their payroll never updated the code. They ended up paying the wrong rates for months, requiring complex adjustments.

HMRC determines your Scottish taxpayer status based on where you spend most nights during the tax year. If you're genuinely unsure because you split time between England and Scotland for work, you need to count nights carefully. Get it wrong, and you'll face either underpayment or overpayment adjustments that disrupt your finances.

National Insurance: The Tax That Isn't Called Tax - Employee National Insurance Reality Check

For 2025/26, employees pay 8% National Insurance on earnings between £12,570 and £50,270, then 2% on anything above. Notice those thresholds align with income tax bands? That's deliberate policy alignment introduced in previous years.

What catches people out is the interaction between NI and income tax. Between £12,570 and £50,270, you're actually paying 28% combined (20% income tax plus 8% NI). If you're a Scottish intermediate rate taxpayer earning £35,000, you're paying 21% income tax plus 8% NI—effectively 29% marginal rate.

The Employer NI Increase Nobody's Talking About

Here's where 2025/26 brings genuine change that affects you indirectly. Employer National Insurance rose from 13.8% to 15%, whilst the secondary threshold (where employers start paying) dropped from £9,100 to £5,000 per employee annually.

Why does this matter to your salary calculation? Because it materially increases employment costs. Some employers, particularly smaller ones or those in competitive sectors, might factor this into salary negotiations, bonus calculations, or whether they can afford pay rises. The total cost of employing you jumped significantly—roughly £800-1,000 extra per year for someone on £30,000.

The £100,000 Trap: When Earning More Costs You More - How the Personal Allowance Withdrawal Works

Let's talk about perhaps the most punitive feature in the UK tax system. Between £100,000 and £125,140, you lose £1 of personal allowance for every £2 earned. This creates an effective marginal tax rate of 60% in England, Wales and Northern Ireland, and 63-64% in Scotland.

Here's the mathematics: earn £110,000, and you've exceeded £100,000 by £10,000. You lose £5,000 of personal allowance (half of £10,000). That £5,000 is now taxed at 40%, costing you an extra £2,000. Combined with the 40% you already pay on that £10,000 (£4,000), plus 2% NI (£200), you're paying £6,200 tax on £10,000 additional income.

Pension Contributions: Your Most Powerful Tool

The most tax-efficient strategy I recommend for clients in the £100,000-£125,140 range is pension contributions. A £10,000 gross pension contribution brings your adjusted net income back to £100,000, restoring your full personal allowance.

Think of it like this: that £10,000 pension contribution saves you approximately £6,200 in tax (the 60% effective rate). You've put £10,000 away for retirement but it only "cost" you £3,800 in reduced take-home. That's a 163% immediate return before any investment growth.

Student Loan Deductions: The Forgotten Tax - Plan Types and Threshold Confusion

Student loans are effectively an additional tax for millions of workers, yet few properly account for them when calculating take-home. For 2025/26, Plan 1 loans (pre-2012 English/Welsh students, current Scottish students) deduct 9% above £24,990. Plan 2 (2012-2023 English/Welsh students) deduct 9% above £27,295. Plan 4 (Scottish post-2007) deduct 9% above £31,395. Plan 5 (post-August 2023) deduct 9% above £25,000. Postgraduate loans deduct 6% above £21,000.

I've seen clients with both undergraduate Plan 2 and postgraduate loans simultaneously repaying 15% (9% + 6%) of income above £27,295. Combined with 20% income tax and 8% NI, their effective marginal rate is 43%—higher than the nominal higher rate tax band.

Why Your Employer Gets This Wrong

Your employer doesn't know which plan you're on unless you tell them or HMRC updates the system. I worked with a teacher who moved from Scotland (Plan 4) to England mid-career. Her employer defaulted to Plan 1, massively overcharging her monthly. She didn't notice for eight months because it was buried in payslip deductions.

Multiple Income Sources: PAYE Meets Self-Employment

The Cumulative Tax Problem

Here's a common scenario: you earn £35,000 PAYE and make £15,000 from freelance work. Your employer taxes you as if £35,000 is your only income, using your full personal allowance. Come January, you realise that £15,000 freelance income is fully taxable at 20%, plus you owe Class 4 NI at 6%.

The calculation: £15,000 at 20% income tax (£3,000) plus 6% Class 4 NI between £12,570-£50,270 on the £15,000 (£900) equals £3,900 due. Many taxpayers in this position haven't budgeted for nearly £4,000 in January because they psychologically see their freelance income as "already earned."

The Tax Code Adjustment Trap

HMRC might adjust your PAYE tax code to collect the previous year's underpayment—let's say that £3,900—through your salary over the year. Your code drops from 1257L to 867L (£3,900 reduction in allowance). Suddenly, each month you're paying an extra £325 in PAYE (£3,900 ÷ 12), and you have no idea why your take-home dropped unless you check your code.

Directors and Dividend Income: The Vanishing Advantage - The Optimal Salary Debate for 2025/26

Company directors historically took small salaries around the NI lower earnings limit (£6,500 in 2025/26) and extracted profits via dividends. This was tax-efficient because dividend tax rates were lower and no NI applied.

For 2025/26, this strategy is under severe pressure. The dividend allowance is just £500 (it was £5,000 in 2022/23). Above £500, dividends are taxed at 8.75% (basic rate), 33.75% (higher rate), and 39.35% (additional rate). If you're a basic rate taxpayer with £20,000 in dividends, you'll pay 8.75% on £19,500 (£1,706.25).

Why Employer NI Changes Matter to You

With employer NI rising to 15% on salaries above £5,000, the cost-benefit calculation has shifted. Taking a £12,570 salary (to use full personal allowance) now costs the company £1,135 in employer NI ([£12,570 - £5,000] × 15%). Previously at 13.8%, this was £1,045—a £90 increase.

Directors need to model whether salary extraction versus dividend extraction makes sense given both personal tax and company-level costs. There's no universal answer, but the sweet spot is narrowing.

Benefits in Kind: The Invisible Additions - Company Cars and the P11D Trap

Your payslip shows your salary, but if you receive a company car, gym membership, or private medical insurance, you're taxed on their cash-equivalent value. This doesn't come out of your bank account—it's collected through a reduced tax code.

Picture this: you earn £45,000 and have a company car with a benefit value of £4,200 annually. Your tax code might be reduced from 1257L to 837L (£4,200 less allowance). This means you pay an extra £84 monthly in tax (£4,200 × 20% ÷ 12) without seeing any corresponding cash deduction.

Why This Confuses Net Pay Calculations

When someone asks, "I earn £45,000—what's my take-home?", the answer depends on whether they have benefits. Two people on £45,000, one with a £5,000 benefit value and one without, have the same gross salary but the first person pays £1,000 more annual tax (£5,000 × 20%). Most salary calculators don't ask about benefits.

Pension Schemes: Relief at Source vs Net Pay - The Tax Relief Method That Changes Everything

This catches people out constantly. Some pension schemes use "relief at source"—you pay from your net salary, the pension provider claims 20% basic rate relief, and higher rate taxpayers claim extra via Self Assessment. Other schemes use "net pay"—contributions come from gross salary before tax.

If you earn £40,000 and contribute £3,000 to a relief-at-source scheme, you physically pay £2,400 (£3,000 - 20%). Your gross salary remains £40,000 for tax purposes. If it's a net pay scheme, your taxable salary becomes £37,000 immediately, and you pay £3,000 from gross.

The Personal Allowance Trap

Here's where it gets strange: if you earn £11,000 and contribute £2,000 to a net pay pension, your taxable income is £9,000—below the personal allowance. You've received no tax benefit. With relief at source, the provider would claim £500 (20% of £2,500 gross contribution), and you'd benefit even though you didn't pay tax.

Low earners in net pay schemes are systematically disadvantaged. HMRC has confirmed this affects around 1.2 million workers, predominantly women in part-time roles. If this is you, consider switching pension schemes or claiming relief directly.

Tax Code Checking: Your First Line of Defence - The HMRC Personal Tax Account Essential

Every UK taxpayer should check their tax code at least three times yearly: April (new tax year), after any job changes, and January (before Self Assessment). Your HMRC Personal Tax Account shows your current code, the assumptions behind it, and estimated tax for the year.

I've identified tens of thousands of pounds in overpayments for clients simply by checking codes. Common errors include: duplicate employment records (HMRC thinks you have two jobs when you don't), outdated benefit values, incorrect state pension coding, and failure to remove previous year adjustments.

The Month-by-Month Reconciliation

Here's a practice that's saved clients significant stress: reconcile your payslip against your expected position monthly. Take your gross annual salary, divide by 12, check that income tax and NI match HMRC's published calculators for cumulative codes.

If your take-home suddenly drops £200 one month with no obvious reason, don't wait—check your tax code immediately. HMRC might have issued a revised code to collect underpayments, and you deserve to know why.

Real Tribunal Cases: Lessons from Tax Disputes - The Scottish Tax Status Dispute (Wilson v HMRC, 2023)

In this First-tier Tribunal case, a consultant worked primarily in London but maintained a flat in Edinburgh where he stayed occasionally. HMRC assessed him as a Scottish taxpayer; he appealed, arguing his main home was England despite the Edinburgh address.

The tribunal examined his diary evidence showing he spent 195 nights in England versus 132 in Scotland (38 nights abroad). They ruled he was not a Scottish taxpayer. The lesson: meticulous night-counting records are essential if your residency is split. The tax difference for someone on £80,000 can exceed £1,500 annually.

Emergency Tax Code Challenges (Multiple Cases 2022-2024)

Several taxpayers successfully challenged HMRC's refusal to refund overpaid tax from emergency codes applied for entire tax years. The key principle established: employers must attempt to obtain a correct code "within a reasonable period" (typically 6-8 weeks).

If you're on an emergency code beyond two months, escalate aggressively. Don't wait for the year-end automatic reconciliation—you may wait 14 months for money that's legally yours.

Practical Calculation: Working Through Real Examples

Example 1: Standard Employee in England

Annual salary: £38,000. Personal allowance: £12,570. Taxable income: £25,430. Income tax: £5,086 (£25,430 × 20%). Employee NI: £2,034.40 ([£38,000 - £12,570] × 8%). Total deductions: £7,120.40. Net annual: £30,879.60 (£2,573.30 monthly).

This assumes no pension, no student loan, no benefits. Add a 5% pension contribution (£1,900 gross), and taxable salary drops to £36,100, reducing tax by £380 annually.

Example 2: Scottish Higher Rate Taxpayer

Annual salary: £60,000 in Scotland. Personal allowance: £12,570. Taxable: £47,430. Tax breakdown: £2,827 × 19% (starter) = £537, £12,093 × 20% (basic) = £2,419, £16,170 × 21% (intermediate) = £3,396, £16,337 × 42% (higher) = £6,862. Total income tax: £13,214. Employee NI: £3,794.40 ([£50,270 - £12,570] × 8% + [£60,000 - £50,270] × 2%). Plan 2 student loan: £2,945 ([£60,000 - £27,295] × 9%). Total deductions: £19,953.40. Net annual: £40,046.60 (£3,337.22 monthly).

Example 3: The £100,000 Trap

Salary: £110,000 in England. Personal allowance: £7,570 (reduced by [£110,000 - £100,000] ÷ 2). Taxable: £102,430. Tax: £37,700 × 20% + £64,730 × 40% = £7,540 + £25,892 = £33,432. Employee NI: £3,989.60 ([£50,270 - £12,570] × 8% + [£110,000 - £50,270] × 2%). Total deductions: £37,421.60. Net: £72,578.40 (£6,048.20 monthly).

Compare to £100,000 salary: Tax £27,432, NI £3,795.60, net £68,772.40. The extra £10,000 gross resulted in only £3,806 extra net—a 38% effective net retention rate, demonstrating the 60%+ marginal rate impact.

Common Mistakes and How to Avoid Them - Assuming Salary Increases Are Linear

The biggest conceptual error is assuming a £5,000 raise means £5,000 more take-home. It doesn't. That £5,000 is taxed at your marginal rate—potentially 20%, 40%, or even 60% depending on your existing income.

A £5,000 raise for someone on £45,000 yields roughly £2,900 extra net (after 20% tax and 8% NI). For someone on £110,000, that same £5,000 might yield only £1,900 net due to the personal allowance taper.

Ignoring Employer Pension Contributions

Many employers contribute to your pension—let's say 5% of salary. This doesn't appear on your take-home calculation, but it's real compensation. Someone on £40,000 with 5% employer contribution is genuinely receiving £42,000 total value, even though they only see £40,000 on their payslip.

When comparing job offers, always gross up the total package including employer pension. A £42,000 role with no pension might be worse than £40,000 with 5% employer contribution (worth £2,000).

Missing Salary Sacrifice Opportunities

Salary sacrifice for pensions, electric cars, or cycle-to-work schemes reduces your gross salary before tax and NI. A £3,000 salary sacrifice pension contribution saves you £840 (20% income tax + 8% NI + 2% NI on remainder) plus potentially £450 employer NI (15%) that employers sometimes share with you.

This is fundamentally different from making pension contributions from net pay. The NI saving alone makes it worthwhile for basic rate taxpayers.

Summary of Key Insights

● Personal allowance remains frozen at £12,570 until April 2028, creating fiscal drag that pulls more earners into higher tax brackets through wage growth alone.

● Scottish taxpayers face six tax bands with rates up to 48%, paying more tax than elsewhere in the UK above approximately £28,850 annual income.

● The £100,000-£125,140 income range creates an effective 60-63% marginal tax rate due to personal allowance withdrawal, making pension contributions critically valuable.

● Employer National Insurance rose to 15% from April 2025 with the threshold dropping to £5,000, significantly increasing employment costs that may affect salary negotiations.

● Emergency tax codes (W1/M1 or X) can cause substantial overpayments lasting months; always provide P45s promptly and monitor tax codes monthly.

● Student loan deductions vary dramatically by plan type, with some borrowers repaying 15% of income above thresholds when combining undergraduate and postgraduate loans.

● Benefits in kind are taxed through reduced tax codes, not payslip deductions, making take-home calculations deceptive without considering P11D values.

● Net pay pension schemes disadvantage low earners who gain no tax relief when contributions reduce income below the personal allowance threshold.

● Tax code errors affect approximately one in seven employees at some point annually; checking your HMRC Personal Tax Account quarterly prevents costly overpayments.

● Multiple income sources require careful planning as PAYE assumes single employment, potentially creating £3,000-£5,000 unexpected Self Assessment liabilities for side earnings.

FAQs

Q1: What happens if someone receives a P800 letter saying they've overpaid tax but never gets the refund?

A1: Well, it's worth noting that P800 letters don't automatically trigger refunds in all cases—you typically need to actively claim through your Personal Tax Account or the HMRC app. In my experience with clients, the key is understanding which type of P800 you've received. If it says you can claim online, you must log in and request the bank transfer yourself; HMRC won't send it automatically. If it mentions a cheque is coming, you should receive it within 14 days of the letter date.

I've seen situations where clients waited months assuming the money would arrive, only to discover they needed to take action. If you've claimed and it's been more than five working days for an online claim or three weeks for a cheque, use HMRC's "Where's My Reply" tool or contact them directly. Sometimes the delay stems from security checks, particularly if you're claiming to a new bank account or if HMRC suspects fraud.

Q2: Can someone split their personal allowance between two part-time jobs to avoid overpaying tax through a BR code?

A2: Yes, you can request this, but here's where I've seen clients slip up—it only makes sense if both jobs pay you relatively stable, predictable amounts throughout the year. Consider a shop assistant in Birmingham I worked with who had two part-time jobs, each paying around £800 monthly. Her second job used code BR, meaning she paid 20% tax on every pound from that job despite her total annual income being well below £25,140. We contacted HMRC to split her £12,570 allowance roughly equally between both employments. The result? Her monthly take-home increased by about £160 because she stopped overpaying tax that would only be refunded the following summer.

However, if your hours fluctuate wildly or you're on zero-hours contracts, splitting can backfire—you might end up underpaying during busy months and owing HMRC money. The safer approach for variable income is to keep BR coding on the second job and claim the refund after year-end.

Q3: How does someone working in England but living in Scotland get taxed, and what happens if their tax code is wrong?

A3: In my experience, this confuses people more than almost any other residency issue. Your tax status depends on where you sleep most nights during the tax year, not where your office is located. If you live in Glasgow but commute to Newcastle for work, you're a Scottish taxpayer and should have an S-prefix code like S1257L. Your employer's location is irrelevant. I've worked with a consultant who moved from London to Edinburgh in October but her employer never updated her tax code—she remained on 1257L until April, paying English rates when she should have paid Scottish rates.

The difference for someone earning £55,000 between October and April meant she underpaid roughly £280. HMRC eventually caught this and adjusted her following year's code to collect the shortfall. If you're genuinely splitting time between Scotland and England, you need to count nights meticulously. Keep a diary or calendar. The threshold is simple: more nights in Scotland means you're Scottish for tax purposes. Check your code includes the S prefix if applicable, and if it doesn't, contact HMRC immediately with evidence of your address.

Q4: What should someone do if they discover they've been on an emergency tax code for an entire tax year?

A4: Right, this is frustrating but surprisingly common, and the good news is that recovery is usually straightforward. Emergency codes like 1257L W1 or M1 tax you on a non-cumulative basis, ignoring the fact that you may have had months earlier in the year with no income or lower earnings. Think of it like this: if you started work in September on £30,000 annually, you should only be taxed on seven months' worth of income, but an emergency code treats each month in isolation. I've seen cases where people overpaid £1,500-£2,500 over a full year.

The employer should have obtained your correct code within 6-8 weeks of you starting. If they didn't and you've been on emergency tax for months, first check your Personal Tax Account to see if HMRC has already calculated a refund—they often reconcile these automatically after the tax year ends and send P800 letters by autumn. If you need the money urgently or the year hasn't ended yet, write to HMRC clearly marked "Repayment Claim," including your P45 from your previous job or explanation of your circumstances, your National Insurance number, and payslips showing the emergency code. Most claims are processed within 8-12 weeks.

Q5: How does someone verify their take-home pay is correct when they have student loan deductions on top of tax and National Insurance?

A5: Let's be honest—student loan deductions are effectively an additional tax that many people completely overlook when calculating take-home, and the complexity has increased dramatically with five different plan types now operating simultaneously. For the 2025-26 tax year, you need to identify which plan applies to you. Plan 1 deducts 9% above £24,990, Plan 2 deducts 9% above £27,295, Plan 4 (Scottish) deducts 9% above £31,395, Plan 5 (post-2023 English students) deducts 9% above £25,000, and postgraduate loans deduct 6% above £21,000. Here's a real scenario I dealt with: a teacher earning £38,000 with both Plan 2 undergraduate and postgraduate loans.

She's repaying 9% on income above £27,295 (£10,705 × 9% = £963.45 annually) plus 6% on income above £21,000 (£17,000 × 6% = £1,020 annually)—that's £1,983.45 in student loans alone, or £165 monthly. Combined with income tax of £5,086 and NI of £2,034, her total annual deductions were £9,103, leaving net pay of £28,897. Most salary calculators don't account for postgraduate loans, so she was initially confused why her take-home was £85 less per month than expected. Always check your payslip shows the correct plan threshold.

Q6: Can someone claim a tax refund for years where they worked only part of the year and didn't use their full personal allowance?

A6: Absolutely, and this is one of the most commonly missed refund opportunities I see, particularly with people who retire mid-year, take career breaks, or leave the UK. Picture this: you worked January to May earning £18,000 total for the year, then stopped working. Your employer applied your tax code as if you'd work the full year, deducting tax on the assumption you'd earn significantly more. You've actually used only £18,000 of your £12,570 personal allowance plus £5,430 in the basic rate band, meaning you should have paid £1,086 in tax (£5,430 × 20%).

But your employer likely deducted more because they didn't know you'd stop working. If you've left work and won't work again before 5 April, you can claim immediately using form P50 rather than waiting for year-end reconciliation. I worked with someone who retired in July having earned £22,000—HMRC refunded her £780 within three weeks of submitting P50. The critical requirement is that you genuinely won't return to employment in that same tax year. If you plan to work again, you'll need to wait for the automatic P800 calculation after April, which typically arrives between June and October.

Q7: Why would someone's take-home pay suddenly drop by several hundred pounds per month with no obvious explanation?

A7: In my experience, this almost always comes down to an unnoticed tax code change, and it catches people completely off-guard because nothing appears different on their payslip initially. Here's a common scenario: HMRC has determined you underpaid tax last year—perhaps you had untaxed income, received benefits in kind that weren't properly coded, or had two jobs where both used your personal allowance. Rather than demanding a lump sum, HMRC adjusts your current tax code to collect the arrears gradually. Let's say you owe £3,600 from last year. Your code might drop from 1257L to 897L (a £3,600 reduction in your allowance). If you're a basic rate taxpayer, that means an extra £720 annual tax deduction (£3,600 × 20%), which translates to £60 per month less in your pocket.

I've seen clients panic when their £2,400 monthly salary suddenly becomes £2,340, and they have no idea why until they actually examine the tax code on their payslip. The solution is to check your Personal Tax Account immediately when take-home drops—look under "Check your Income Tax" to see why your code changed and whether you can challenge it. Sometimes HMRC's calculation is based on incorrect information. If the deduction creates genuine financial hardship, you can contact HMRC to negotiate spreading it over a longer period.

Q8: What happens to someone's tax position if they switch from full-time PAYE employment to self-employment mid-year?

A8: This transition creates a tax reconciliation situation that genuinely requires careful planning, because you're moving from a system where tax is automatically deducted to one where you're responsible for calculating and paying it yourself. Consider someone I advised who worked January to August as an employee earning £24,000, then went fully self-employed from September onwards, earning £18,000 in profit by April. During employment, their employer deducted roughly £2,286 in income tax (assuming they used the full £12,570 allowance across eight months). Here's the complexity: when you complete your Self Assessment return for the full tax year, HMRC looks at your total income—£42,000 in this case.

Your personal allowance of £12,570 has already been applied during employment, so the remaining £29,430 is taxable. The £24,000 employment income has been taxed, but the £18,000 self-employment profit is untaxed. You'll owe £3,600 in income tax on that £18,000 (20% rate), plus Class 4 National Insurance at 6% on the amount between £12,570 and £50,270—roughly £1,080 additional NI. Many people transitioning to self-employment don't budget for this £4,680 liability that comes due by 31 January. Set aside approximately 26-28% of your self-employment profit to cover both income tax and NI contributions, and consider making payments on account if you know you'll remain self-employed.

Q9: How does someone check if they're being overtaxed due to having a company car or other benefits in kind?

A9: Benefits in kind create a silent tax drain that most people don't even realize is happening because nothing comes directly out of your bank account—it's all done through a reduced tax code. Let me walk you through how this works. Your employer reports the cash-equivalent value of benefits like company cars, private medical insurance, or gym memberships to HMRC via a P11D form. HMRC then reduces your tax code to collect tax on these benefits throughout the year. For example, imagine you earn £42,000 and have a company car valued at £5,400 annually (this depends on the car's list price, CO2 emissions, and fuel type—electric cars have much lower percentages).

Your tax code should drop from 1257L to 717L (£5,400 less allowance). As a 20% taxpayer, this means you pay an extra £1,080 annually (£5,400 × 20%), or £90 monthly. Now, here's where I've seen errors: sometimes the benefit value is calculated incorrectly—perhaps your employer reported the wrong car model or didn't account for your contribution towards private fuel. Other times, you might have returned the car or benefit but HMRC never updated your code. Check your Personal Tax Account under "Company Benefits" to see what HMRC thinks you're receiving. If it's wrong, contact your employer's payroll first to correct the P11D, then notify HMRC once it's amended.

Q10: Can someone claim a refund on National Insurance contributions if they have multiple jobs that both pay above the threshold?

A10: Yes, but the mechanism is quite specific and different from income tax refunds, and it's something I find people overlook entirely because they don't realize the NI system works differently. Unlike income tax where you have one personal allowance across all employment, NI is calculated separately for each job. The threshold for 2025-26 is £12,570 annually. If you have two jobs each paying £20,000, you're paying 8% NI on roughly £7,430 per job (£20,000 - £12,570), totaling about £1,189 in NI across both jobs. Here's the thing: there's a maximum NI contribution limit. If your combined earnings from all employments exceed £50,270, you may be entitled to an NI refund on the excess amount subject to the 8% rate versus the 2% rate.

However, the refund isn't automatic like tax refunds can be. You need to apply to HMRC specifically for a National Insurance refund using form CA5609 after the tax year ends. I worked with a healthcare worker who had three part-time nursing jobs totaling £58,000 annually. She discovered she'd overpaid roughly £500 in NI because the multiple employers didn't coordinate. HMRC refunded her within 12 weeks of applying. This is particularly relevant if you've changed jobs multiple times in one tax year or work multiple part-time roles simultaneously.

About the Author:

Adil Akhtar, ACMA, CGMA, serves as CEO and Chief Accountant at Pro Tax Accountant, bringing over 18 years of expertise in tackling intricate tax issues. As a respected tax blog writer, Adil has spent more than three years delivering clear, practical advice to UK taxpayers. He also leads Advantax Accountants, combining technical expertise with a passion for simplifying complex financial concepts, establishing himself as a trusted voice in tax education.

Email: adilacma@icloud.com

Disclaimer:

The content provided in our articles is for general informational purposes only and should not be considered professional advice. Pro Tax Accountant strives to ensure the accuracy and timeliness of the information but makes no guarantees, express or implied, regarding its completeness, reliability, suitability, or availability. Any reliance on this information is at your own risk. Note that some data presented in charts or graphs may not be 100% accurate.

We encourage all readers to consult with a qualified professional before making any decisions based on the information provided. The tax and accounting rules in the UK are subject to change and can vary depending on individual circumstances. Therefore, PTA cannot be held liable for any errors, omissions, or inaccuracies published. The firm is not responsible for any losses, injuries, or damages arising from the display or use of this information.

.png)