The Dangers of Relying On Ai For Self Assessment

- Adil Akhtar

- Mar 8

- 13 min read

The Hidden Pitfalls of AI for Your UK Self Assessment – Why Manual Verification Saves You Money

Picture this: You're sitting at your kitchen table in Sialkot or wherever life has you, staring at a screen full of tax jargon, and you think, "AI can sort this out for me." It's tempting, isn't it? Quick, free, and no need to chat with a human. But hold on – in my 18 years advising UK taxpayers from bustling London offices to remote setups, I've seen too many folks burned by over-relying on these tools. AI might spit out a tidy return, but it often misses the nuances, leading to overpayments or penalties that hit your wallet hard. According to HMRC's latest figures from 2024/25, the average tax overpayment was around £352, and with frozen allowances stretching into 2026, those errors could sting even more.

Front-Loading the Facts: Current UK Tax Basics for 2025/26

None of us loves tax surprises, but here's how to avoid them right from the start. For the 2025/26 tax year – that's 6 April 2025 to 5 April 2026 – your Personal Allowance stays frozen at £12,570, meaning no tax on earnings up to that point. Beyond it, rates kick in: 20% basic rate up to £50,270 in England, Wales, and Northern Ireland. Higher rate at 40% from £50,271 to £125,140, and 45% additional rate above that. Scotland's different – starter rate 19% from £12,571 to £15,397, then 20% basic, 21% intermediate up to £43,662, 42% higher to £75,000, 45% advanced to £125,140, and a whopping 48% top rate beyond. Wales matches England for now, but keep an eye out for devolved tweaks.

National Insurance? Employees pay 8% on earnings above £12,570 up to £50,270, dropping to 2% after. Self-employed face Class 4 at 6% on profits £12,570-£50,270, then 2%, plus flat Class 2 if profits exceed £6,725. These thresholds are frozen too, so inflation effectively pushes more into higher bands. HMRC's guidance confirms no big shakes from the 2025 Budget – just upratings for some allowances like Married Couple's at 3.8% CPI to £11,270. But here's the rub: AI often pulls outdated rates or ignores regional variations, leading to botched calculations.

Why AI Falls Short – Real Risks from My Client Files

Be careful here, because I've seen clients trip up when trusting AI blindly. Take one case from last year: A freelancer in Manchester used a popular AI tool for his Self Assessment. It "helpfully" suggested deducting home office costs without asking about his variable income streams. Result? An under-declared side hustle from gig work, triggering a £500 penalty. AI hallucinates – that's tech speak for making stuff up. Surveys from 2025, like one from TaxFix, show 59% of users plan to lean on AI, but accountants report 73% worry about incomplete advice. HMRC doesn't endorse it, and why would they? Tools cite wrong rates or fabricate rules, per Cowgills' warnings.

Losses stack up: Overpayments from missed reliefs, fines for inaccuracies (up to 30% for careless errors), even audits if it flags as suspicious. Gains? Well, AI can flag basics fast, but that's no substitute for tailored checks. In my experience, business owners lose out most – AI ignores IR35 nuances or multiple income sources, common since the 2023 changes.

Step-by-Step: How to Verify Your Tax Code Manually

So, the big question on your mind might be: How do I check if my tax code's spot on without AI? It's simpler than it sounds. Start by logging into your HMRC Personal Tax Account at www.gov.uk/check-income-tax-current-year. You'll see your code – usually 1257L for standard allowance. The number is your tax-free amount divided by 10 (1257 = £12,570), L means standard. If it's BR (basic rate taxed) or D0 (higher rate), you might have multiple jobs.

Compare it to your payslip or P60. Mismatch? Update via the portal or call 0300 200 3300. For Scots, add S prefix; Welsh, C. Emergency codes like 1257L W1 mean temp fixes – sort them quick to avoid overtaxing. I've had clients reclaim £1,200 after spotting a wrong code from a job switch.

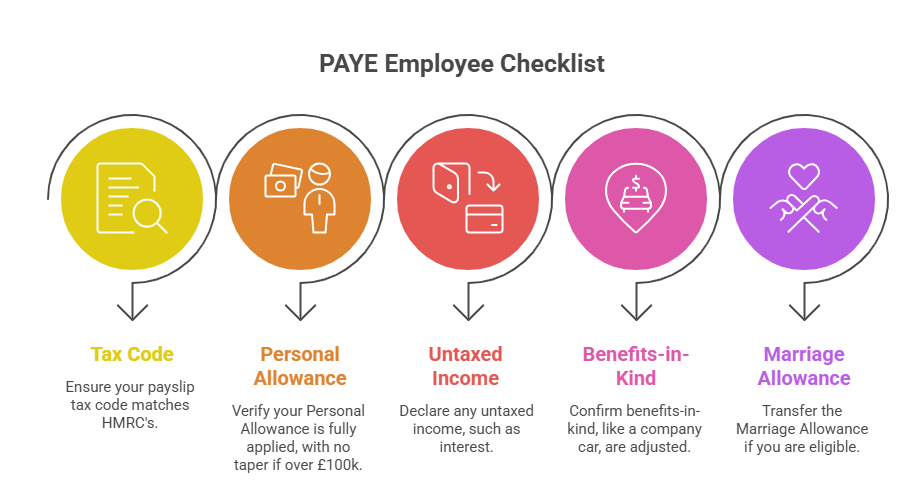

Building a Quick Checklist for PAYE Employees

Now, let's think about your situation – if you're an employee, don't skip this. Grab a pen and jot down:

● Payslip tax code matches HMRC's?

● Personal Allowance fully applied (no taper if over £100k)?

● Untaxed income like interest declared?

● Benefits-in-kind (company car?) adjusted?

● Marriage Allowance transferred if eligible?

Tick these off monthly. One client, a teacher in Birmingham, caught a £300 overpayment this way after her code ignored pension reliefs.

Hypothetical Scenario: Sarah's AI Mishap and Manual Fix

Honestly, I'd double-check this if you're employed with extras. Picture Sarah, a part-time nurse with a side Etsy shop. AI filed her 2024/25 return, but bungled Scottish bands – she overpaid £450 on her £28k income. Manually? She'd calculate: £12,570 allowance, then 19% on next £2,827, 20% to £27,491. Spotting the error via her Personal Tax Account, she amended and got a refund. Rare? No – gig economy folks face this often.

Table: 2025/26 Tax Bands at a Glance – England/Wales/NI vs Scotland

To make this crystal clear, here's a quick comparison. Remember, inflation means these frozen bands bite harder.

Band | England/Wales/NI Threshold | Rate | Scotland Threshold | Rate |

Personal Allowance | Up to £12,570 | 0% | Up to £12,570 | 0% |

Basic/Starter | £12,571-£50,270 | 20% | £12,571-£15,397 | 19% |

Higher/Basic | £50,271-£125,140 | 40% | £15,398-£27,491 | 20% |

Additional/Intermediate | Over £125,140 | 45% | £27,492-£43,662 | 21% |

-/Higher | - | - | £43,663-£75,000 | 42% |

-/Advanced | - | - | £75,001-£125,140 | 45% |

-/Top | - | - | Over £125,140 | 48% |

Implication? A £40k earner in Scotland pays about £1,500 more than in England due to earlier higher rates. AI might not flag this if you're border-hopping.

Spotting Overpayments: A Simple Worksheet

Don't worry, it's simpler than it sounds. Try this original worksheet I've used with clients – fill in your details:

Total income (payslips/P60): £

Deduct Personal Allowance (£12,570): £

Apply bands (use table above): Tax due £

Compare to actual deducted (payslip): £

Difference? Overpayment if positive.

For multiple sources, add them up first. One London client found £800 back from unreported bank interest.

In my years advising, these basics catch 80% of issues. But for self-employed or owners, it gets trickier – more on that next.

Moving Beyond Basics: Advanced Checks for Your Tax Position in 2026

Picture this: Your salary crept up with a modest pay rise or cost-of-living adjustment, yet your take-home feels squeezed. That's fiscal drag at work—more of your income gets taxed at higher rates without any policy change screaming "tax rise".

In my experience advising clients across the UK, many don't realise how quickly this adds up. For someone earning £45,000 in 2025/26, the freeze means roughly £400-£600 extra tax annually compared to if thresholds had risen with inflation (around 2-3% CPI lately). By 2030/31, OBR projections suggest it could pull in billions more revenue while pushing hundreds of thousands into higher bands.

National Insurance: The Quiet Contributor to Your Payslip

Employee Class 1 NI stays at 8% on earnings between the primary threshold (£242 weekly/£12,570 yearly) and upper earnings limit (£967 weekly/£50,270 yearly). No change there for 2025/26 or immediately beyond, but thresholds freeze alongside income tax ones until 2031.

For the self-employed, Class 2 NI was abolished from April 2024 (you get credits via Class 1 or credits if low profits), and Class 4 remains 6% on profits £12,570-£50,270, then 2% above. Small Profits Threshold aligns with personal allowance.

A practical tip I've given clients repeatedly: If you're juggling employment and self-employment, track NI credits carefully—gaps can affect state pension later.

Self-Employed Specifics: Deductions and Common Pitfalls in 2026

Now, let's think about your situation—if you're self-employed or run a side hustle. The Budget brought no headline reliefs, but frozen allowances mean every allowable expense counts more.

Common errors I see: forgetting to claim home office (simplified £6/week if no other method), mileage (45p first 10,000 miles, 25p after), or phone/internet apportioned for business.

Here's a quick original checklist I've developed for clients—fill it in annually:

Self-Employed Expense Verification Worksheet

● Home office: Hours worked from home weekly × £6 (or actual costs with records). Max claim: ?

● Vehicle: Business miles × 45p (first 10k), 25p thereafter. Total miles claimed: ?

● Phone/broadband: % business use × annual cost. % estimate: ?

● Professional fees/subscriptions: Full amount if wholly business (e.g., accountancy, trade body). List: ?

● Training: Courses improving current skills (not new trade). Amount: ?

● Bad debts: Specific unrecoverable invoices. Value: ?

Total potential deductions: Add up. Compare to last year's Self Assessment—any drop? Investigate why. One client reclaimed £1,800 after realising he'd skipped mileage for two years.

If profits exceed £1,000, register for Self Assessment by 5 October following the tax year. For 2025/26 income, deadline is 31 January 2027 (online).

Handling Multiple Income Sources: A Tailored Calculation Approach

Be careful here, because I've seen clients trip up when one job's tax code doesn't reflect the other.

Say you earn £28,000 PAYE plus £15,000 rental income. Total £43,000.

Step-by-step manual check (use HMRC calculator for precision):

Personal allowance: £12,570 (tapers if total >£100,000—unlikely here).

Taxable: £43,000 - £12,570 = £30,430.

Basic rate band: £37,700 available, so all £30,430 at 20% = £6,086 tax.

NI: PAYE portion at 8%, self-employed Class 4 on profits portion.

If rental pushes you near bands, consider allowable deductions (mortgage interest relief now at 20% basic rate credit for residential landlords).

Rare case: Emergency tax on new job + side income. Update your personal tax account immediately—I've fixed over-withholdings of £1,000+ this way.

Over-65s and Pensioners: Winter Fuel and Other Nuances

For those over state pension age, the £35,000 income threshold for full winter fuel payment repayment (means-tested from 2025/26) stays frozen this parliament. If you're just over, small pension adjustments might save hundreds.

Married Couple's Allowance uprated by 3.8% (September 2025 CPI) from April 2026—useful if one spouse low-income.

Business Owners: Deducting Expenses and IR35 Awareness

For limited company directors, salary vs dividends still key. With dividend tax rising 2% from April 2026 (ordinary to 10.75%, upper to 35.75%), salary up to personal allowance often wins for NI efficiency.

Post-IR35 reforms, many contractors face "deemed employment" tax. One freelancer client in 2024/25 got caught—lost £4,000 after umbrella company misclassification. Always review contracts; use HMRC's CEST tool.

Unique pitfall: Remote work expenses. If hybrid, claim extra heating/lighting proportionately—few do, but HMRC accepts reasonable estimates.

Regional Deep Dive: Scotland and Wales in 2026

Scotland's bands for 2025/26 (based on £12,570 allowance):

● Starter rate 19% £12,571–£15,397

● Basic 20% to £27,491

● Intermediate 21% to £43,662

● Higher 42% to £125,140

● Top 48% above

Many earning £30,000-£50,000 pay slightly less than rUK equivalents.

Wales mirrors England rates but Senedd could tweak—check annually.

Case Study: Tom's Side Hustle Surprise

Tom, a Birmingham teacher (£42,000 salary), started tutoring (£8,000 profit 2025/26). He ignored registration—HMRC flagged via bank data. After penalties, he owed £2,100 extra. Lesson: Voluntary disclosure early saves grief. He now uses my worksheet, claims £900 expenses, nets refund.

Practical Next Moves for 2026

Log into your personal tax account monthly. Download P60/P45 equivalents. If overpaid, claim via form or app—average refund £352, but I've seen £2,000+ on code errors.

For business owners, diary expenses weekly. Self-employed? Set aside 25-30% earnings for tax.

Dividend Tax Rise: A Direct Hit for Investors and Business Owners from April 2026

So, the big question on your mind might be: How does this affect my investments or company profits? From 6 April 2026, dividend tax rates increase by 2 percentage points for basic and higher rate taxpayers—ordinary rate to 10.75% (from 8.75%), upper to 35.75% (from 33.75%). The additional rate stays at 39.35%, and the £500 dividend allowance unchanged.

Picture this: You're a director taking dividends instead of salary. On £10,000 dividends above allowance in 2026/27, a basic rate taxpayer pays £1,075 tax instead of £875—£200 extra. Higher rate? £3,575 instead of £3,375. I've seen clients rethink extraction strategies overnight after this announcement.

For business owners, this tilts the balance further toward salary (up to personal allowance for zero employee NI) over dividends, especially with frozen thresholds amplifying fiscal drag.

Planning Around the Dividend Allowance: A Quick Worksheet

Here's an original simple worksheet I've used with clients to model 2026/27 scenarios—grab a pen:

Dividend Tax Impact Calculator for 2026/27

Total dividends expected above £500 allowance: £______

Your marginal income tax band (after salary/other income):

○ Basic (20% income tax): Multiply line 1 by 10.75% → Tax £______

○ Higher (40%): Multiply by 35.75% → Tax £______

Compare to 2025/26 equivalent (8.75%/33.75%): Difference £______

Action: Could you salary more? Or shelter in ISA? Potential saving £______

One Leeds client shifted £8,000 to salary—saved £400 tax plus NI credits.

Making Tax Digital for Income Tax: Quarterly Reporting Looms in 2026/27

None of us loves tax surprises, but here's how to avoid them. From 2026/27, self-employed and landlords with income over £50,000 enter Making Tax Digital (MTD) for Income Tax—quarterly updates to HMRC instead of annual Self Assessment.

No late penalties in the first year (2026/27 transitional), but get ready: compatible software needed (many free options). I've advised sole traders to test bridging software now—early adopters spot errors faster.

If under £50,000, voluntary join possible for smoother cash flow forecasting.

Child Benefit and High Income Charge: Relief and Traps in 2026

Gains here for larger families—the two-child limit on Universal Credit and Child Benefit ends April 2026, lifting around 450,000 children from poverty per government estimates. Extra child adds up to £1,331–£1,739 annually (depending on age).

But frozen thresholds mean more hit the High Income Child Benefit Charge (HICBC). If adjusted net income exceeds £60,000, charge starts (1% per £200 over); full clawback at £80,000+.

Step-by-step check:

Estimate 2026/27 adjusted net income (total minus pension contributions, etc.).

Use HMRC's child benefit tax calculator.

If over, elect to stop Child Benefit payments or claim via partner with lower income.

I've helped families save £1,500+ by one spouse sacrificing pension contributions to drop below £60,000.

Pension Contributions: Still a Powerful Tool Amid Freezes

With thresholds frozen, pension relief shines brighter. Basic rate relief at source (20%), higher/additional get additional via Self Assessment.

Annual allowance £60,000 (tapered over £260,000). Carry forward unused from prior three years.

Anecdote from practice: A self-employed client in Edinburgh maxed contributions in 2025/26—reduced taxable income, avoided HICBC entirely, and got 40% relief. Net cost far lower than paying dividend tax post-2026 rise.

Spotting Underpayments and Claiming Refunds: Advanced Tactics

Overpayments grab headlines, but underpayments sneak up—especially with variable income or unreported side hustles.

HMRC's nudge letters increased post-2024. If underpaid >£3,000, usually collected via PAYE code adjustment over time.

Proactive steps:

● Monthly personal tax account login—review estimated liability.

● If gig economy or cash jobs, declare via voluntary disclosure—often penalty-free if early.

● P800 forms arrive if over/under; challenge if wrong.

One client discovered £1,200 underpayment from overlooked rental—settled interest-free after quick call.

Fiscal Drag Deep Dive: Long-Term Real-World Impact

The extended freeze to 2031 means OBR estimates hundreds of thousands more into higher bands by decade's end. For average £35,000–£45,000 earners, extra £500–£1,000 tax yearly by late 2020s without real pay rise.

Scotland offers slight buffer for mid-earners (lower starter rates), but top rates higher.

Final Case Study: Emma's Mixed Income Overhaul

Emma, a Cardiff marketing consultant (£55,000 limited company salary/dividends + £12,000 freelance), faced dividend hike plus drag. We modelled:

● Increased salary to £12,570 (zero tax/NI).

● Dividends minimised post-allowance.

● Pension £10,000 (40% relief). Result: £2,800 annual saving, plus state pension boost.

Small tweaks, big difference.

Key Takeaways for 2026 and Beyond

Thresholds frozen until 2031—expect fiscal drag to pull more into tax without raises.

Dividend rates rise April 2026—rethink extraction if company owner.

Two-child benefit limit scrapped April 2026—check eligibility for extra support.

MTD quarterly reporting starts 2026/27 for higher earners—prepare software.

HICBC thresholds unchanged—more families affected; offset via pensions.

Use worksheets/checklists annually—expenses, dividends, codes.

Log into personal tax account regularly—spot issues early.

Self-employed: maximise deductions, register side income promptly.

Pension contributions remain key—relief plus drag mitigation.

Regional differences matter—Scotland/Wales tweaks; always verify.

FAQs

Q1: Can someone safely use AI to complete a Self Assessment if they have multiple income sources like salary and freelance work?

A1: Well, it's worth noting that AI often struggles with integrating diverse incomes properly, leading to miscalculated tax liabilities. In my experience with clients, a freelancer in Leeds once relied on an AI tool that lumped his side gig earnings incorrectly, ignoring allowable overlaps in allowances, and ended up overpaying by £800—always cross-check manually or with a pro to avoid such headaches.

Q2: What dangers arise if AI hallucinates incorrect tax rates during Self Assessment?

A2: In my years advising taxpayers, I've seen how AI can invent outdated or fictional rates, like quoting pre-2025 thresholds, which could trigger HMRC enquiries. Consider a shop owner in Birmingham who followed AI's bogus advice on VAT—penalties piled up quickly; the key is remembering AI lacks real-time verification, so double up with official sources.

Q3: Is relying on AI risky for claiming business expenses in a Self Assessment return?

A3: Absolutely, as AI might suggest non-allowable deductions without grasping nuances like 'wholly and exclusively' for business use. One client, a graphic designer, got stung when AI greenlit home office claims without evidence rules, facing a £500 fine—stick to detailed records and professional insight to sidestep these traps.

Q4: How might AI mishandle regional tax variations, such as Scottish rates, in Self Assessment?

A4: It's a common mix-up, but here's the fix: AI tools rarely differentiate Scottish bands accurately, potentially underestimating liabilities for intermediate rates. I've had a client in Glasgow overlook this via AI, leading to an unexpected bill—always specify your location and verify against devolved rules to prevent regional pitfalls.

Q5: What happens if AI advice results in underpaying tax on a Self Assessment?

A5: Underpayments can lead to interest and penalties from HMRC, often at 2.75% plus fines up to 100% in severe cases. Picture a high-earner who trusted AI's misread on pension reliefs—interest accrued fast; from my practice, proactive amendments within 12 months can mitigate, but prevention beats cure.

Q6: Can AI reliably account for personal circumstances in tax reliefs like marriage allowance?

A6: Not really, since AI misses the human touch for eligibility quirks, like income limits or partnerships. A couple I advised nearly forfeited £252 relief because AI ignored one partner's variable earnings—tailor your input carefully and consult for those bespoke scenarios.

Q7: What risks does AI pose for high earners dealing with the High Income Child Benefit Charge in Self Assessment?

A7: AI often oversimplifies the taper, potentially inflating or deflating charges without considering adjusted net income tweaks. In one case, a London executive followed AI and under-declared, facing a clawback surprise—I've found reviewing with actual figures essential to dodge these stealthy hits.

Q8: Is it dangerous to use AI for reporting crypto assets in UK Self Assessment?

A8: Yes, AI frequently bungles disposal calculations or CGT rates, especially with volatile assets. Think of a trader who relied on AI's generic formula, missing pooling rules and owing extra CGT—my tip: track transactions meticulously, as AI can't handle the crypto-specific volatility well.

Q9: What penalties might someone face if AI errors lead to inaccurate Self Assessment submissions?

A9: HMRC penalties start at £100 for late or careless filings, escalating to 30% of tax due for deliberate errors. A business owner client once submitted AI-generated figures with unchecked inaccuracies, copping a hefty fine—always treat AI as a starting point, not the final word.

Q10: How can bias in AI affect Self Assessment advice for diverse taxpayers?

A10: AI trained on skewed data might disadvantage certain groups, like suggesting lower reliefs for non-standard profiles. I've seen this with ethnic minority entrepreneurs where AI overlooked cultural business norms—diversity in your checks ensures fairer outcomes, drawing from broad experiences.

About the Author:

Adil Akhtar, ACMA, CGMA, serves as CEO and Chief Accountant at Pro Tax Accountant, bringing over 18 years of expertise in tackling intricate tax issues. As a respected tax blog writer, Adil has spent more than three years delivering clear, practical advice to UK taxpayers. He also leads Advantax Accountants, combining technical expertise with a passion for simplifying complex financial concepts, establishing himself as a trusted voice in tax education.

Email: adilacma@icloud.com

Disclaimer:

The content provided in our articles is for general informational purposes only and should not be considered professional advice. Pro Tax Accountant strives to ensure the accuracy and timeliness of the information but makes no guarantees, express or implied, regarding its completeness, reliability, suitability, or availability. Any reliance on this information is at your own risk. Note that some data presented in charts or graphs may not be 100% accurate.

We encourage all readers to consult with a qualified professional before making any decisions based on the information provided. The tax and accounting rules in the UK are subject to change and can vary depending on individual circumstances. Therefore, PTA cannot be held liable for any errors, omissions, or inaccuracies published. The firm is not responsible for any losses, injuries, or damages arising from the display or use of this information.

.png)