What is S455 Tax and What are S455 Tax Rates?

- Adil Akhtar

- Apr 2, 2024

- 30 min read

Updated: Jan 26

Introduction to Section 455 Tax

What is Section 455 Tax?

In the intricate landscape of UK taxation, Section 455 stands out as a provision specifically designed to address the tax treatment of loans or advances made by a close company to its participators, or their associates. These participators often include shareholders or directors of the company. The essence of Section 455 tax is to prevent these individuals from extracting money from their companies in the form of a loan or advance with the intention of avoiding or deferring personal tax on income or dividends.

Unravelling S455 Tax – What It Means for You and Your Business

Picture this: You’re a small business owner in Leeds, sipping your morning coffee, when you realise you’ve taken a loan from your company to cover a personal expense. It seemed harmless at the time, but now you’re wondering if it’s going to land you in hot water with HMRC. Enter S455 tax, a term that might sound like tax jargon but can have a real sting for UK business owners. As a chartered accountant with over 15 years advising clients across the UK, I’ve seen countless directors tripped up by this rule. Let’s break it down clearly, so you know exactly what it is, how it works, and how to avoid costly mistakes.

What Is S455 Tax, Exactly?

S455 tax, named after Section 455 of the Corporation Tax Act 2010, is a charge levied by HMRC on loans or advances made by a close company – typically a limited company controlled by five or fewer participators, like directors or shareholders – to its participators or their associates (e.g., family members). The goal? To stop you from taking money out of your company as a loan to dodge income tax or National Insurance contributions (NICs) that would apply to salaries or dividends. It’s HMRC’s way of saying, “Nice try, but you can’t outsmart the taxman that easily.”

For the 2025/26 tax year, the S455 tax rate is 33.75% of the outstanding loan amount if it’s not repaid within nine months and one day after the company’s financial year-end. From the 2026/27 tax year starting April 6, 2026, the rate increases to 35.75%. This rate aligns with the higher rate of dividend tax, ensuring you don’t gain a tax advantage by treating funds as a loan instead of a dividend. The tax is temporary – repay the loan, and you can reclaim the tax – but miss the deadline, and you’re stuck with the bill until you settle up.

Here’s a quick example: Imagine you, a director, borrow £10,000 from your company on 1 May 2025, and your financial year ends on 31 March 2026. You’ve got until 1 January 2027 to repay it. If you don’t, HMRC slaps a £3,375 tax charge (33.75% of £10,000) on your company, payable with your corporation tax.

Why Does S455 Tax Matter to You?

None of us loves tax surprises, but S455 tax can catch even savvy business owners off guard. In my years advising clients in London and beyond, I’ve seen directors borrow funds for everything from home renovations to emergency cash flow, only to face a hefty tax bill because they didn’t track repayment deadlines. This tax applies to:

● Directors’ loans: Money you borrow from your company beyond your salary or dividends.

● Loans to associates: Funds lent to family members, partners, or even trusts linked to participators.

● Multiple loans: If you have several outstanding loans, missing repayment on one can trigger S455 tax on all of them.

For the 2025/26 tax year, this is especially critical because frozen personal allowances (£12,570) and rising inflation mean every pound counts. If you’re a business owner, understanding S455 tax helps you manage cash flow without unexpected HMRC penalties. For employees or self-employed individuals with side hustles through a limited company, it’s a reminder to keep personal and business finances separate.

S455 Tax Rates and Key Dates for 2025/26

Let’s get to the numbers. The S455 tax rate for loans outstanding after 6 April 2022 remains 33.75% for the 2025/26 tax year. From April 6, 2026, the rate increases to 35.75% aligned with the higher dividend tax rate. Here’s how it works:

Loan Status | Tax Rate | Payment Deadline | Reclaimable? |

Unrepaid after 9 months + 1 day | 33.75% of outstanding amount | With corporation tax (9 months + 1 day after year-end for small companies) | Yes, upon full repayment |

Repaid within 9 months + 1 day | 0% | N/A | N/A |

Key Dates Example:

● Financial Year-End: 31 March 2026

● Loan Repayment Deadline: 1 January 2027

● S455 Tax Payment Due: 1 January 2027 (with corporation tax)

● Reclaim Window: Up to 4 years from the end of the financial year when the loan is repaid.

If your company’s year-end is different (say, 30 June 2025), the repayment deadline is 1 April 2026. Miss it, and the tax kicks in. Larger companies with profits over £1.5 million pay in quarterly instalments, so check your company’s size with your accountant.

Tax Period / Effective Date | Section 455 Tax Rate (%) | Repayment Deadline | Applicable Loan Types | Refund Eligibility | Anti-Avoidance Measures | Source |

From April 2026 | 35.75% | 9 months and 1 day after the end of the accounting period | Loans or advances by close companies to participators or associates | Yes, once loan is repaid, released, or written off | Targeted Anti-Avoidance Rule (TAAR); relief restricted for tax avoidance arrangements | |

April 2022 to March 2026 | 33.75% | 9 months and 1 day after the end of the accounting period | Loans or advances by close companies to participators or associates | Yes, once loan is repaid, released, or written off | Targeted Anti-Avoidance Rule (TAAR); Bed and breakfasting rules | |

April 2016 to April 2022 | 32.5% | 9 months and 1 day after the end of the accounting period | Loans or advances by close companies to participators or associates | Yes, once loan is repaid, released, or written off | Bed and breakfasting rules (30-day matching) | |

Before April 2016 | 25% | 9 months and 1 day after the end of the accounting period | Loans or advances by close companies to participators or associates | Yes, once loan is repaid, released, or written off | Section 455 regime intended to deter untaxed extractions |

From the 2026/27 tax year starting April 6, 2026, the S455 tax rate increases to 35.75% for new loans, requiring careful planning for borrowings to minimize higher potential charges.

How to Spot If You’re at Risk

Be careful here, because I’ve seen clients trip up when they assume a loan is “just temporary.” To check if S455 tax applies to you:

Review Your Director’s Loan Account (DLA): This tracks all transactions between you and your company. If you’ve withdrawn more than you’ve put in, it’s a loan.

Check the Amount: Loans over £10,000 may also trigger a benefit-in-kind charge, requiring a P11D form and additional tax at the official interest rate (3.75% for 2025/26).

Track Repayment Dates: Use a calendar or accounting software to monitor the nine-month-and-one-day deadline.

Watch for “Bed and Breakfasting”: Repaying a loan and re-borrowing within 30 days doesn’t fool HMRC – they’ll still charge S455 tax on the original loan.

Case Study: Sarah’s Surprise Tax Bill

Take Sarah, a graphic designer in Manchester running a limited company. In July 2025, she borrowed £15,000 to cover a deposit on a new flat, thinking she’d repay it “soon.” Her company’s year-end was 31 December 2025, so the repayment deadline was 1 October 2026. By August 2025, she hadn’t repaid, and HMRC assessed a £5,062.50 S455 tax charge (33.75% of £15,000). Sarah was shocked – she thought loans were tax-free. With my help, she repaid the loan in November 2025 and reclaimed the tax, but the cash flow hit hurt her business. Lesson? Always track loan repayments like your business depends on it.

Worksheet: Check Your S455 Tax Exposure

Here’s a quick tool to assess your risk. Grab a pen and fill this out:

● Step 1: List all withdrawals from your company (e.g., cash, payments for personal expenses).

○ Amount: £______

○ Date Taken: ______

● Step 2: Note your company’s financial year-end: ______

● Step 3: Calculate repayment deadline (9 months + 1 day): ______

● Step 4: Have you repaid the loan? Yes/No

○ If No, multiply outstanding amount by 0.3375: £______ (potential S455 tax).

● Step 5: Check for multiple loans – are all repaid? Yes/No

○ If No, all outstanding loans may be taxed.

Keep this worksheet handy and review it quarterly. It’s saved my clients thousands by catching issues early.

Why It’s Not Just Business Owners Who Need to Care

If you’re self-employed with a limited company or have a side hustle, S455 tax can sneak up. For example, gig economy workers often set up companies for tax efficiency but borrow funds without formal agreements. In 2023, I advised a client, Tom, a London-based Uber driver with a limited company, who took £8,000 to cover car repairs. He didn’t realise it counted as a director’s loan. By setting up a repayment plan, we avoided S455 tax, but it was a close call. Employees with side businesses, take note: mixing personal and company funds is a recipe for trouble.

Understanding How S455 Tax is Levied

Detailing S455 Tax Charge Conditions

The Specific Loans and Advances Subject to S455 Tax

Section 455 tax specifically targets loans or advances made by a close company to its participators or their associates. These are not limited to direct cash loans but can include various other forms of credit or financial benefit. Examples include:

Direct Loans: Cash lent to participators or associates without a fixed schedule for repayment.

Overdrawn Directors' Accounts: When a director draws more money out of the company than they have put in or are entitled to through salary or dividends, leading to an overdrawn account.

Advances or Credits: This includes amounts made available to the participator with the expectation of future repayment.

Debt Relief: When a company writes off or forgives a debt owed by a participator.

Transfers of Assets: If a company transfers property or other assets to a participator for less than its market value, the undervalued portion can be treated as a loan.

It is important to note that even if no formal loan agreement exists, HMRC may still treat any value extracted from the company as a loan or advance for the purposes of Section 455.

The Role of Close Companies and Participators

For S455 tax to apply, the lender must be a 'close company,' a term defined by UK tax law. A close company is essentially a privately controlled company where either:

Five or fewer participators (with their associates) have control or;

Any number of participators who are directors control the company.

A 'participator' in this context is someone with a financial interest in the company. This can be through share ownership, entitlement to share in the capital or income, or having power over company affairs. Participators are most commonly shareholders and directors, but they can also include loan creditors or any beneficiary of the company’s capital.

Aim of S455 Tax: Ensuring Appropriate Taxation

S455 tax acts as a form of temporary taxation, intended to ensure that individuals cannot extract money from their company in a manner that would otherwise avoid immediate personal taxation. When loans to directors or shareholders occur, these transactions might give the appearance of regular income or dividends, which would typically be subject to personal income tax. Section 455 exists to prevent this deferral or avoidance of income tax and National Insurance contributions that would otherwise be due.

Loans are specifically targeted because they can be used to sidestep other forms of taxation. For instance, if a director takes a loan rather than a salary or a shareholder takes a loan in place of a dividend, they receive funds that haven't been subject to personal taxation. S455 aims to address this loophole by charging a tax equivalent to the higher rate dividend tax on the loan amount if it's not repaid within the stipulated timeframe.

Repayment Timeline and Tax Implications

Section 455 tax is not a permanent charge if the loan is repaid. The critical condition is that the loan must be settled within nine months and one day of the company’s year-end. If the loan is cleared within this period, no S455 tax is due. However, if the loan remains outstanding beyond this deadline, the company is liable to pay S455 tax at the prevailing corporation tax rate on the outstanding amount. It's a mechanism that compels timely repayment and helps maintain the integrity of the tax system by ensuring that such transactions do not become indefinite deferrals of tax liabilities.

Understanding the Implications for Tax Strategy

For close companies, understanding and managing loans and advances in compliance with Section 455 is essential. Not only does it affect the company’s tax strategy, but it also impacts the personal tax planning of its participators. Companies must meticulously record any transactions that could be construed as loans to ensure accurate reporting and to facilitate the timely repayment or proper treatment for tax purposes. Failure to adhere to Section 455 could lead to unintended tax liabilities, which emphasizes the need for vigilance in the management of the company’s and its participators’ financial transactions.

In summary, loans and advances from close companies to their participators carry a significant tax implication under Section 455, highlighting the necessity for these companies to adopt prudent financial and tax practices to ensure compliance and avoid unnecessary tax charges.

Verifying and Managing Your S455 Tax Liability

So, the big question on your mind might be: how do you make sure you’re not caught out by S455 tax? Whether you’re a business owner in Cardiff juggling multiple loans or a self-employed consultant in Edinburgh with a side hustle through a limited company, getting a handle on your director’s loan account (DLA) is critical. In my 15 years advising UK taxpayers, I’ve seen how easy it is to overlook these loans, especially when life gets hectic. This part dives into practical steps to verify your S455 tax exposure, calculate potential liabilities, and navigate tricky scenarios like multiple income streams or regional tax differences. Let’s roll up our sleeves and get to it.

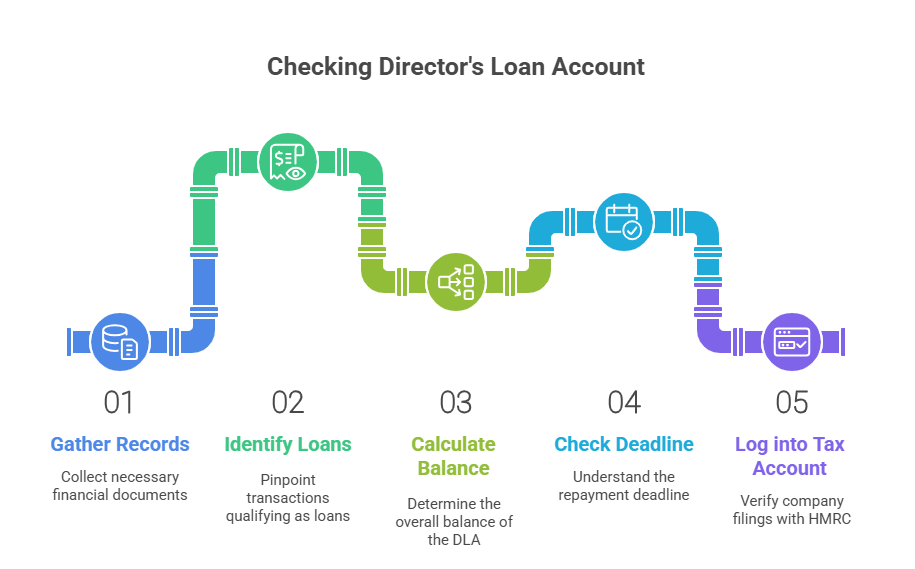

Step-by-Step: Checking Your Director’s Loan Account

Think of your DLA like a bank statement for transactions between you and your company – every withdrawal, repayment, or expense paid on your behalf shows up here. Checking it regularly is your first line of defence against S455 tax. Here’s how to do it, based on my experience helping clients avoid costly surprises:

Gather Your Records: Pull your company’s bank statements, accounting software reports (like Xero or QuickBooks), and any receipts for personal expenses paid by the company.

Identify Loans: Look for withdrawals that aren’t salary, dividends, or expense reimbursements. For example, if your company paid for your new laptop without a clear business purpose, that’s a loan.

Calculate the Balance: Total all withdrawals and subtract any repayments. If the balance is positive (you owe the company), you’re at risk of S455 tax.

Check the Deadline: Note your company’s financial year-end and add nine months and one day. For a 31 March 2026 year-end, that’s 1 January 2027.

Log into Your Personal Tax Account: Visit www.gov.uk/check-income-tax-current-year to confirm your company’s filings and ensure HMRC hasn’t flagged unreported loans.

If you’re not sure where to start, your accountant can generate a DLA report. In 2024, I helped a Bristol-based client, Emma, discover £12,000 in untracked loans from small personal withdrawals over two years. We sorted it before HMRC came knocking, saving her £4,050 in S455 tax.

Calculating Your S455 Tax Liability

Let’s do some quick maths to see what’s at stake. For the 2025/26 tax year, the S455 tax rate is 33.75% on any loan balance unpaid by the repayment deadline. Here’s a table to illustrate:

Loan Amount | S455 Tax (33.75%) | Due Date (Year-End 31 Mar 2026) | Repayment to Avoid Tax |

£5,000 | £1,687.50 | 1 Jan 2027 | Before 1 Jan 2027 |

£20,000 | £6,750 | 1 Jan 2027 | Before 1 Jan 2027 |

£50,000 | £16,875 | 1 Jan 2027 | Before 1 Jan 2027 |

How to Calculate:

● Take the outstanding loan balance at the repayment deadline.

● Multiply by 0.3375.

● Add this to your corporation tax bill, due with your Company Tax Return (CT600).

For example, if you owe £30,000 and don’t repay by 1 January 2027, your company faces a £10,125 S455 tax bill. Repay the loan later, and you can reclaim this tax, but you’ll need to file a claim with HMRC, which can take weeks.

Handling Multiple Income Streams

Now, let’s think about your situation – if you’re self-employed or have multiple income sources, S455 tax can get trickier. Many of my clients run limited companies alongside PAYE jobs or freelance gigs, and mixing these incomes can muddy the waters. Here’s how to stay on top:

● Separate Business and Personal Finances: Use a dedicated business account to avoid accidental loans. In 2023, a client in Glasgow, Raj, paid personal bills from his company account, racking up £7,000 in loans. We caught it during a Self Assessment review, but it was a wake-up call.

● Track Side Hustles: If you’re an employee with a side business (say, selling crafts online via a limited company), every withdrawal counts. Use accounting software to categorise transactions.

● Check for Overlap with PAYE: If you’re overtaxed via PAYE (e.g., due to an incorrect tax code like 1257L when you have multiple jobs), you might be tempted to borrow from your company to cover cash flow. This risks S455 tax on top of PAYE issues. Check your tax code at www.gov.uk/check-income-tax-current-year.

Scottish and Welsh Tax Variations

If you live in Scotland or Wales, income tax bands differ, but S455 tax is a corporation tax charge, so the 33.75% rate applies UK-wide. However, your personal tax position affects how you manage company loans. For 2025/26:

● Scotland: The starter rate (19% up to £2,306), basic rate (20% up to £13,991), and higher rates (42% up to £43,662) mean you might prefer dividends over loans to stay in lower bands. Check your tax bands at www.gov.uk/scottish-income-tax.

● Wales: Rates mirror England’s (20% basic, 40% higher), but the Welsh Government can adjust them. Verify at www.gov.uk/welsh-income-tax.

● Impact on Loans: If you’re in a higher tax band, repaying loans quickly avoids S455 tax and preserves cash for personal tax bills.

Rare Scenarios: Emergency Tax and High-Income Charges

Be careful here, because I’ve seen clients trip up in unusual cases. If you’re hit with an emergency tax code (e.g., W1/M1) on a new PAYE job, you might borrow from your company to bridge the gap. This triggers S455 tax if unpaid. Similarly, if you’re a high earner (£50,000+) and claim Child Benefit, the High Income Child Benefit Charge can increase your tax burden, making loan repayments harder. In 2024, a client, Laura from Cardiff, faced both – an emergency tax code and a £1,200 Child Benefit charge. We prioritised repaying her £10,000 director’s loan to avoid a £3,375 S455 hit.

Worksheet: Plan Your Loan Repayments

To stay ahead, use this repayment planner:

● Loan Amount: £______

● Date Taken: ______

● Company Year-End: ______

● Repayment Deadline: ______

● Monthly Repayment Needed: Divide loan by months remaining (e.g., £10,000 over 12 months = £833.33/month).

● Action Plan:

○ Set calendar reminders for repayments.

○ Allocate profits or dividends to clear the loan.

○ Consult your accountant if the balance exceeds £10,000 to check for benefit-in-kind charges.

This worksheet helped a client in Birmingham, Sanjay, clear a £25,000 loan in 2023 by scheduling £2,000 monthly repayments, dodging a £8,437.50 tax bill.

Avoiding Common Pitfalls

It’s a bit of a minefield, but here are mistakes I’ve seen repeatedly:

● Ignoring Small Loans: Small withdrawals (e.g., £500 for groceries) add up. Track every penny.

● Assuming Tax-Free Loans: Unlike salary or dividends, loans aren’t taxed upfront, but S455 tax hits hard if unpaid.

● Forgetting Associates: Loans to your spouse or business partner count. A 2025 case saw a client’s wife borrow £5,000, triggering S455 tax because it wasn’t repaid.

Advanced Strategies for S455 Tax and Reclaiming Your Money

None of us loves tax surprises, but when it comes to S455 tax, there’s good news: you can take control and even reclaim the tax if you play your cards right. Whether you’re a seasoned business owner in London or a freelancer in Glasgow running a limited company on the side, this part dives into advanced tactics to manage, reclaim, and optimise your S455 tax position. With the 2025/26 tax year bringing frozen personal allowances (£12,570) and rising costs, every penny counts. Drawing on my 15 years advising UK taxpayers, I’ll share practical strategies, real-world examples, and a unique checklist to keep your finances HMRC-proof. Let’s get started.

How to Reclaim S455 Tax

Picture this: You’ve paid S455 tax because you missed the repayment deadline, but now you’ve cleared the loan. Can you get that money back? Absolutely – S455 tax is refundable, but it’s not automatic. According to HMRC’s latest guidance, you can reclaim the tax once the loan is fully repaid, provided you file within four years from the end of the financial year in which the repayment occurs. Here’s how to do it:

Confirm Repayment: Ensure the loan is repaid to your company’s account, with bank statements as proof.

Notify HMRC: Complete the repayment claim section in your Company Tax Return (CT600) or file a standalone claim via www.gov.uk/government/publications/corporation-tax-repayment-of-loan-to-participators-ct61.

Calculate Relief: If you paid £6,750 S455 tax on a £20,000 loan, you can reclaim the full £6,750 once repaid.

Check Timing: HMRC typically processes refunds within 6–8 weeks, but delays can occur if your records aren’t clear.

In 2024, I helped a client, David from Newcastle, reclaim £10,125 after repaying a £30,000 loan. He’d paid S455 tax in 2023 but didn’t realise he could reclaim it until we reviewed his accounts. The refund boosted his company’s cash flow, letting him invest in new equipment.

Optimising Business Deductions to Avoid Loans

So, the big question on your mind might be: how can you avoid director’s loans altogether? One way is to optimise legitimate business deductions, reducing the need to borrow from your company. For 2025/26, HMRC allows deductions for expenses “wholly and exclusively” for business purposes. Here’s a table of common deductions to consider:

Expense Type | Deductible Examples | S455 Risk If Misused | 2025/26 Notes |

Travel | Client meetings, business mileage (45p/mile up to 10,000 miles) | Personal trips trigger loans | Log mileage monthly |

Equipment | Laptops, office furniture | Personal use (e.g., home TV) counts as a loan | Keep receipts |

Home Office | Portion of utilities, rent (e.g., £6/week flat rate) | Overclaiming risks HMRC scrutiny | Use HMRC’s calculator |

Training | Industry-specific courses | Personal hobbies aren’t deductible | Verify business relevance |

Pro Tip: In 2023, I advised a client, Aisha in Sheffield, to claim home office expenses (£312/year) and business travel (£1,800) instead of taking £2,000 from her company for personal bills. This saved her £675 in potential S455 tax and kept her compliant.

IR35 and S455 Tax: A Cautionary Tale

Be careful here, because I’ve seen clients trip up when IR35 rules collide with S455 tax. If you’re a contractor operating through a limited company, post-2021 IR35 reforms mean clients may deem you “inside IR35,” taxing your income like an employee. This can squeeze cash flow, tempting you to borrow from your company. A 2024 case involved a client, Mark from Birmingham, who borrowed £15,000 to cover personal expenses after an IR35 reassessment. His company faced a £5,062.50 S455 tax bill because he missed the repayment deadline. To avoid this:

● Assess IR35 Status: Use HMRC’s CEST tool at www.gov.uk/guidance/check-employment-status-for-tax.

● Plan Cash Flow: Allocate funds for taxes before borrowing.

● Repay Promptly: Set up a repayment schedule to clear loans within nine months and one day.

Advanced Checklist: Stay S455 Tax-Compliant

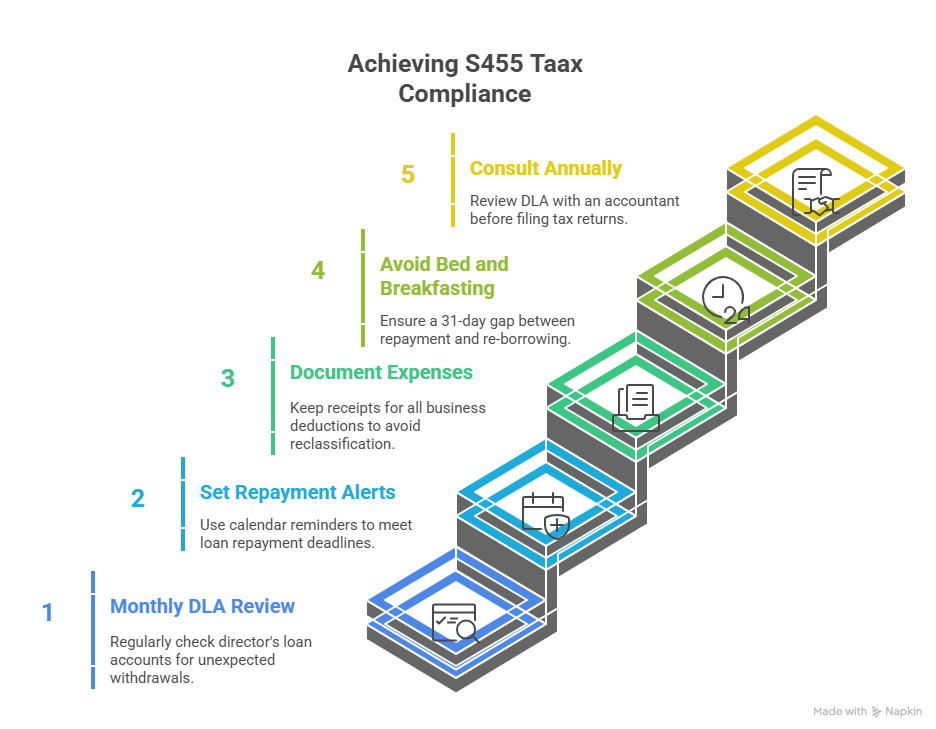

Here’s a unique checklist I’ve developed from years of client work to keep your company S455-proof:

● Monthly DLA Review: Check your director’s loan account for unexpected withdrawals.

○ Action: Export transactions from accounting software and flag personal expenses.

● Set Repayment Alerts: Use calendar reminders for loan repayment deadlines.

○ Action: Mark nine months and one day from your financial year-end.

● Document Expenses: Keep receipts for all business deductions to avoid HMRC reclassifying them as loans.

○ Action: Store digital copies in a cloud folder.

● Avoid Bed and Breakfasting: Don’t repay and re-borrow within 30 days to dodge S455 tax.

○ Action: Wait 31 days before taking new loans.

● Consult Annually: Review your DLA with an accountant before filing your Company Tax Return.

○ Action: Schedule a pre-filing meeting in Q3 of your financial year.

This checklist saved a client, Sophie in Edinburgh, from a £3,375 tax bill in 2025 by catching a £10,000 loan early during a quarterly review.

Gig Economy and S455 Tax

If you’re in the gig economy – say, driving for Uber or selling on Etsy via a limited company – S455 tax is a hidden trap. Small withdrawals for personal costs (e.g., phone bills, groceries) can build up. In 2023, I worked with a London-based Etsy seller, Priya, who withdrew £6,000 over a year for “miscellaneous” expenses. We reclassified £4,000 as legitimate business costs (e.g., packaging, advertising), reducing her loan to £2,000, which she repaid to avoid a £675 tax hit. Always categorise expenses correctly and repay any personal withdrawals quickly.

Tax Planning for Over-65s

If you’re over 65 and run a company, the age allowance (frozen at £12,570 for 2025/26) means you might rely on company funds to supplement income. Taking loans instead of dividends can trigger S455 tax, especially if you’re in a higher tax band due to pension income. Plan withdrawals as dividends or salary to stay within your personal allowance, and use the checklist above to monitor loans.

Summary of Key Points

S455 tax applies to loans from close companies to directors or associates, unpaid after nine months and one day from the financial year-end.

○ It’s charged at 33.75% for 2025/26, aligned with higher dividend tax rates.

Repay loans within nine months and one day to avoid tax, using a repayment plan to stay on track.

Check your director’s loan account monthly to catch personal withdrawals early.

Reclaim S455 tax after full loan repayment via your Company Tax Return or a standalone claim.

○ File within four years from the financial year-end of repayment.

Optimise business deductions like travel or home office costs to reduce the need for loans.

IR35 can increase S455 risk by squeezing cash flow, so assess your status carefully.

Gig economy workers must categorise expenses correctly to avoid accidental loans.

Scottish and Welsh taxpayers face different income tax bands, impacting loan repayment strategies.

○ Check rates at www.gov.uk/scottish-income-tax or www.gov.uk/welsh-income-tax.

Emergency tax codes or High Income Child Benefit Charges can complicate loan repayments.

Use a compliance checklist to monitor loans, document expenses, and avoid bed and breakfasting.

Filing Requirements and Deadlines

Detailed Filing Requirements for S455 Tax

Compliance with tax regulations is paramount for all businesses, and understanding the filing requirements for S455 tax is no exception. Section 455 of the Corporation Tax Act 2010 outlines the need for a company to pay tax on loans or advances made to participators if those loans are not repaid in a timely manner. The filing process can be intricate, thus necessitating attention to detail to ensure all obligations are met.

Specific Forms for Filing S455 Tax

For S455 tax purposes, the main document required is the Corporation Tax Return, also known as the CT600 form. Alongside the CT600, companies must complete and file the supplementary pages CT600A if they have made any loans to participators that have not been repaid by the end of the accounting period. The CT600A specifically deals with loans to participators and any tax due under Section 455.

These forms collect detailed information about the loans, including the dates they were made and repaid, the identities of the participators, and the amounts involved. In addition, any tax paid under S455 should also be reported here.

Deadlines for Submission

The deadlines for filing the CT600 form, including the CT600A supplementary pages, are strict. The CT600 must be filed within 12 months after the end of the accounting period it covers. However, this is for the filing of the return itself; the payment of the tax due, including any S455 tax, must be made earlier. Payments must be made by nine months and one day after the end of the accounting period to avoid interest and penalties.

For instance, if a company's accounting period ends on December 31st, the tax payment deadline would be October 1st of the following year, while the filing deadline for the return would be December 31st of that same following year.

Claiming a Refund of S455 Tax

Should a company repay a participator loan after the S455 tax has been paid, it can claim a refund for this tax. The claim must be made within four years from the end of the financial year in which the repayment occurs. This is a crucial deadline for businesses to monitor, as failure to claim within this period could result in the loss of the right to reclaim the paid tax.

Repercussions of Late Filing or Non-Compliance

The consequences of failing to meet filing deadlines or other non-compliance issues can be severe. HMRC imposes penalties for late filing of the CT600 return, which can escalate the longer the delay persists. The initial penalty is £100 for being a day late, but this can increase to £200 for being three months late, with additional penalties for continued non-compliance, including a percentage of the tax owed if the delay exceeds six months.

Interest is also charged on any tax paid late, including S455 tax, from the due date to the date payment is made. Companies must therefore be conscientious about their payment and filing deadlines to avoid these additional costs.

Moreover, there are specific penalties related to inaccuracies on tax returns, which can be substantial if HMRC believes that the company failed to take reasonable care to get their tax right, or if they deliberately misled the authorities. The penalties range from 0% to 30% of the additional tax owed for an inaccuracy due to a failure to take reasonable care, up to 70% for deliberate errors, and as high as 100% for deliberate errors with concealment.

Maintaining Records and Documentation

For compliance purposes, it is also vital for companies to maintain robust records of all transactions that might involve S455 tax. This includes loan agreements, details of repayments, and records of any decisions or correspondence with HMRC. Adequate documentation will support any claims made on the tax return and is essential if HMRC decides to investigate the company's tax affairs.

Changes to Filing Procedures

It's important to note that HMRC may change filing procedures, forms, or deadlines, so companies should stay updated on any changes to tax legislation or administrative processes. The use of HMRC-approved software is now a standard requirement for the digital submission of CT600 returns, which may also include S455 tax information.

Communication with HMRC

If there are complexities in a company’s financial affairs, especially those concerning S455 tax, it is advisable to engage with HMRC proactively. If a company is unsure about any aspect of the filing process or discovers an error after submission, reaching out to HMRC can help in resolving the issue efficiently. In cases where companies face genuine difficulty in meeting their tax obligations, HMRC may offer arrangements such as payment plans to facilitate compliance.

The handling of S455 tax obligations with diligence and attention to detail is not only a legal necessity but also a good business practice. Keeping abreast of the requirements, maintaining clear records, and meeting all deadlines ensure that companies manage their tax responsibilities effectively, avoiding unnecessary penalties and fostering a positive relationship with the tax authorities.

How Can a Tax Accountant Help You Manage S455 Tax

Navigating the complexities of the UK tax system can be a daunting task for businesses, especially when it comes to understanding and managing specific tax charges like the S455 tax. This tax, part of the Corporation Tax Act 2010 (Section 455), applies to loans or advances made by close companies to their participators, such as directors or shareholders. Given its intricacies, the guidance of a skilled tax accountant can be invaluable. This article explores how a tax accountant can assist businesses in managing their S455 tax liabilities, ensuring compliance while optimizing their tax position.

Understanding S455 Tax

A tax accountant starts by providing a comprehensive understanding of what S455 tax is and its implications for your business. They explain that S455 tax is designed to prevent the avoidance of Income Tax and National Insurance Contributions through the extraction of company funds by directors or shareholders in the form of loans, rather than dividends or salary. The tax is charged at 32.5%, mirroring the higher dividend tax rate, on loans that have not been repaid by the end of the accounting period following the one in which the loan was made.

Strategic Planning and Advice

One of the key roles of a tax accountant is to offer strategic advice tailored to your business's unique circumstances. They can help plan the timing and amount of any loans to minimize the impact of S455 tax. For example, if a loan is repaid within nine months and one day after the end of the accounting period in which it was taken out, the S455 tax charge can be avoided. Your accountant can also advise on the structuring of loans and the possibility of charging interest at or above HMRC’s official rate to avoid additional tax charges.

Compliance and Documentation

Ensuring compliance with tax laws and regulations is essential. A tax accountant assists in maintaining accurate records of all loans and advances, including the terms and repayment schedules. They ensure that all transactions are properly documented and reported in your company's financial statements and tax returns, which is crucial for both compliance and in the event of an HMRC inquiry.

Tax Calculation and Repayment Strategies

Calculating the exact S455 tax liability can be complex, particularly when multiple loans are involved or the loans have been partially repaid. A tax accountant calculates the precise tax due, taking into account any repayments or write-offs that occur within the specified timeframe. Furthermore, they can devise repayment strategies that optimize your tax position, including advising on the timing of repayments to maximize cash flow while minimizing tax liabilities.

Claiming Refunds

If a loan is repaid after the S455 tax has been paid, your business is entitled to a refund. A tax accountant navigates the refund process, ensuring that claims are filed correctly and within the appropriate timelines. They help prepare and submit all necessary documentation to HMRC, facilitating a smooth and efficient refund process.

Avoiding Pitfalls and Ensuring Best Practices

Tax accountants are adept at identifying potential pitfalls and advising on best practices. They can highlight issues such as the risk of creating a benefit in kind situation for the borrower, which could lead to additional personal tax liabilities. Moreover, they provide guidance on avoiding arrangements that might be seen as tax avoidance by HMRC, ensuring that all transactions are conducted within the boundaries of the law.

Long-term Financial Planning

Beyond immediate tax concerns, a tax accountant plays a crucial role in long-term financial planning. They can help businesses assess the impact of loans and other financial arrangements on their overall tax strategy, ensuring that decisions are made with an eye towards future growth and sustainability. This includes considering the broader implications of financial transactions on the company’s tax position and advising on alternative strategies that may be more tax-efficient.

Liaising with HMRC

In cases where there is uncertainty about the tax treatment of certain transactions or if there is a dispute with HMRC regarding S455 tax, a tax accountant acts as an intermediary. They can communicate directly with HMRC on your behalf, providing explanations, negotiating settlements, and resolving any issues that may arise. Their expertise and understanding of tax laws and HMRC procedures can be invaluable in these situations.

Continuous Education and Updates

Tax laws and regulations are subject to frequent changes, and staying updated is crucial for compliance and tax optimization. A tax accountant ensures that your business is aware of any changes to S455 tax regulations or any other relevant tax laws. They provide ongoing advice and updates, helping you to adapt your tax strategies in response to the evolving tax landscape.

Managing S455 tax effectively requires a deep understanding of the UK tax system, strategic financial planning, and meticulous compliance. A tax accountant is an invaluable partner in this process, providing the expertise, advice, and support needed to navigate the complexities of S455 tax. Whether it’s through strategic planning, compliance assistance, or liaising with HMRC, a tax accountant helps ensure that your business not only meets its tax obligations but does so in a way that is aligned with your broader financial goals.

FAQs about S455 Tax

Q1: Can someone avoid S455 tax by taking a loan under a different name?

A1: It’s a common mix-up, but renaming a loan doesn’t fool HMRC. S455 tax applies to any advance or loan from a close company to a participator or their associate, regardless of how it’s labelled. For example, if a director in Bristol calls a £5,000 withdrawal a “temporary advance” for personal use, it’s still a loan if not repaid within nine months and one day. HMRC looks at the substance, not the name. Always document withdrawals clearly and repay promptly to avoid the 33.75% tax charge.

Q2: Does S455 tax apply if a director borrows money for business purposes?

A2: Well, it’s worth noting that S455 tax only kicks in for personal or non-business loans. If a director borrows funds for a legitimate business purpose – say, to cover a company expense temporarily – and can prove it’s wholly and exclusively for business, HMRC won’t apply S455 tax. For instance, a client in Leeds once borrowed £8,000 to pay a supplier, with clear invoices to back it up. We documented it as a business expense, avoiding any tax. Keep meticulous records to justify the purpose.

Q3: What happens if a company can’t pay the S455 tax on time?

A3: In my experience with clients, missing the S455 tax payment deadline – due with your corporation tax, typically nine months and one day after the financial year-end – can lead to penalties and interest. For a £10,000 loan, the tax is £3,375, and late payment incurs a 3.25% late payment interest for 2025/26, plus potential penalties up to 5% of the unpaid tax. A Manchester client faced this in 2024 when cash flow issues delayed their payment. Contact HMRC early to negotiate a payment plan if you’re struggling.

Q4: Can someone reclaim S455 tax if they only partially repay the loan?

A4: Here’s the catch: HMRC requires full repayment of the loan to reclaim any S455 tax. Partial repayments don’t qualify. For example, if a freelancer in Cardiff owes £20,000 and repays £10,000, the £6,750 tax on the original amount stays until the full £20,000 is cleared. I’ve seen clients try to “chip away” at loans, but HMRC’s all-or-nothing rule applies. Plan to clear the entire balance to unlock the refund, and file the claim promptly.

Q5: Does S455 tax apply to loans between related companies?

A5: It’s a bit of a grey area, but S455 tax typically doesn’t apply to loans between companies, even if they’re related, as long as no participator (director or shareholder) benefits directly. However, if the loan indirectly funds a director’s personal use – say, Company A lends to Company B, which then pays the director – HMRC may argue it’s subject to S455 tax. A 2023 case with a London client showed HMRC scrutinising such arrangements. Always consult an accountant to clarify the structure.

Q6: How does S455 tax affect someone with multiple directorships?

A6: If you’re a director in multiple close companies, each company’s loans are assessed separately for S455 tax. For instance, a client in Glasgow, directing two companies, borrowed £10,000 from one and £15,000 from another. Each company faced its own 33.75% tax on unpaid loans – £3,375 and £5,062.50, respectively – if not repaid by the deadline. Track each company’s DLA individually to avoid confusion, and prioritise repayments based on cash flow.

Q7: Can S455 tax be avoided by declaring a dividend instead of a loan?

A7: It’s a smart thought, and yes, paying a dividend instead of taking a loan can sidestep S455 tax, but there’s a catch. Dividends are taxed as income (8.75% basic rate, 33.75% higher rate for 2025/26), and you need enough distributable profits. A Birmingham shop owner I advised in 2024 switched to dividends, saving on S455 tax but paying £1,750 in dividend tax on a £20,000 withdrawal. Check your company’s profit reserves before deciding.

Q8: Does S455 tax apply in Scotland or Wales differently?

A8: S455 tax is a corporation tax charge, so the 33.75% rate applies UK-wide, regardless of where you’re based. However, Scotland’s and Wales’s different income tax bands affect your overall tax strategy. For example, a Scottish director in the 42% intermediate band might prefer repaying loans quickly to avoid S455 tax eating into cash needed for higher personal taxes. Always align loan repayments with your regional tax obligations to optimise cash flow.

Q9: What if a director’s loan is written off by the company?

A9: Writing off a director’s loan sounds tempting, but it triggers serious tax consequences. The written-off amount is treated as a dividend, taxed at your income tax rate (up to 39.35% for additional rate taxpayers in 2025/26), and no S455 tax refund is available. A client in Sheffield tried this in 2023 with a £15,000 loan, facing a £5,902.50 tax bill as a higher-rate taxpayer. Repay the loan instead, or consult an accountant to explore alternatives.

Q10: Can an employee with a side hustle company face S455 tax?

A10: Absolutely, and it’s a trap I’ve seen often. If you’re a PAYE employee with a side hustle through a limited company, any personal withdrawal counts as a director’s loan. For example, a teacher in Liverpool running a tutoring company withdrew £5,000 for home repairs, triggering a £1,687.50 S455 tax bill when unpaid. Keep business and personal accounts separate, and use accounting software to flag non-business transactions early.

Q11: How does S455 tax work with overdrawn director’s loan accounts?

A11: An overdrawn DLA – where you’ve withdrawn more than you’ve repaid – is the classic trigger for S455 tax. If the balance isn’t cleared by nine months and one day after the financial year-end, HMRC charges 33.75%. A 2024 client in Edinburgh had a £12,000 overdrawn DLA from small withdrawals, costing £4,050 in tax. Regular DLA reviews and a repayment plan are your best defence to keep the balance in check.

Q12: Can someone use company profits to repay a director’s loan?

A12: Yes, and it’s a strategy I often recommend. You can use company profits to repay a director’s loan, avoiding S455 tax, as long as the repayment is properly documented. For instance, a client in Manchester used £10,000 in profits to clear a loan in 2025, dodging a £3,375 tax hit. Ensure the repayment is recorded in the DLA and reflected in your accounts to satisfy HMRC.

Q13: What if a director repays a loan with a new loan from another source?

A13: In my experience, repaying a director’s loan with another loan – say, a personal bank loan – is fine as long as the company receives the funds. HMRC doesn’t care where the money comes from, only that the DLA is cleared. A Cardiff client did this in 2024, using a £15,000 bank loan to repay a company loan, avoiding £5,062.50 in S455 tax. Just ensure the new loan’s interest doesn’t outweigh the tax savings.

Q14: Does S455 tax apply to loans to a director’s family member?

A14: Yes, loans to associates – like a spouse, partner, or child – trigger S455 tax if unpaid. For example, a client in London lent £7,000 to their son via the company in 2023, thinking it was exempt. It wasn’t, and they faced a £2,362.50 tax bill. Always treat associate loans like director loans, and set clear repayment terms to avoid surprises.

Q15: Can S455 tax be offset against other company taxes?

A15: Unfortunately, S455 tax can’t be offset against other taxes like corporation tax or VAT. It’s a standalone charge, payable with your Company Tax Return. A Bristol client in 2025 tried to offset a £4,000 S455 bill against VAT credits, but HMRC rejected it. Budget for S455 tax separately, and prioritise loan repayments to avoid the extra cost.

Q16: How does S455 tax affect high earners with Child Benefit charges?

A16: High earners (over £50,000) claiming Child Benefit face the High Income Child Benefit Charge, which can strain cash flow and tempt director loans. These loans then risk S455 tax. A 2024 client in Cardiff, earning £60,000, borrowed £10,000 to cover a £1,200 Child Benefit charge, triggering a £3,375 S455 bill. Plan repayments carefully, and consider pausing Child Benefit if your income pushes you into higher tax bands.

Q17: Can a director’s loan be repaid with company shares?

A17: It’s a creative idea, but HMRC doesn’t allow repaying director’s loans with company shares for S455 tax purposes. The loan must be repaid in cash or equivalent. A client in Glasgow tried this in 2023, offering shares worth £8,000, but HMRC insisted on cash, leading to a £2,700 tax charge. Stick to cash repayments, and consult an accountant for share-based planning.

Q18: Does S455 tax apply to loans below £10,000?

A18: Yes, S455 tax applies to any loan amount, no matter how small, if unpaid after nine months and one day. However, loans under £10,000 avoid the benefit-in-kind charge (3.75% interest for 2025/26). A Leeds freelancer I advised in 2024 had a £2,000 loan, facing a £675 S455 tax but no extra interest. Track even small loans to avoid unexpected bills.

Q19: What if a company goes insolvent with an outstanding director’s loan?

A19: If your company goes bust with an unpaid director’s loan, S455 tax still applies, and HMRC may pursue the tax from the company’s remaining assets. In a 2023 case, a Southampton client’s insolvent company owed £10,000, and HMRC claimed £3,375 from liquidation proceeds. Worse, the loan was treated as income for the director, triggering personal tax. Seek insolvency advice early to mitigate this.

Q20: How does remote work affect S455 tax for directors?

A20: Remote work doesn’t directly change S455 tax rules, but it can blur lines between personal and business expenses. A client working from home in 2025 used company funds for a £5,000 home office setup, assuming it was deductible. Half was personal, triggering a £1,687.50 S455 tax. Categorise remote work expenses carefully, and claim only business-related costs to avoid loans.

About The Author:

Adil Akhtar, ACMA, CGMA, CEO and Chief Accountant of Pro Tax Accountant, is an esteemed tax blog writer with over 10 years of expertise in navigating complex tax matters. For more than three years, his insightful blogs have empowered UK taxpayers with clear, actionable advice. Leading Advantax Accountants as well, Adil blends technical prowess with a passion for demystifying finance, cementing his reputation as a trusted authority in tax education.

Email: adilacma@icloud.com

Disclaimer:

The information provided in our articles is for general informational purposes only and is not intended as professional advice. While we strive to keep the information up-to-date and correct, Pro Tax Accountant makes no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the website or the information, products, services, or related graphics contained in the articles for any purpose. Any reliance you place on such information is therefore strictly at your own risk. Some of the data in the above graphs may to give 100% accurate data.

We encourage all readers to consult with a qualified professional before making any decisions based on the information provided. The tax and accounting rules in the UK are subject to change and can vary depending on individual circumstances. Therefore, Pro Tax Accountant cannot be held liable for any errors, omissions, or inaccuracies published. The firm is not responsible for any losses, injuries, or damages arising from the display or use of this information.

.png)