Why HMRC Reopens Landlord Tax Returns

- Adil Akhtar

- Apr 3

- 9 min read

Understanding HMRC's Enquiry Powers for Landlord Tax Returns

The Surprise Letter from HMRC

Picture this: you've filed your self-assessment tax return as a landlord, everything seems in order, and months or even years pass without a peep. Then, out of the blue, a letter arrives from HMRC stating they're opening an enquiry. It's a scenario I've encountered countless times in my 18 years advising UK taxpayers. Often, it's not malice but a simple mismatch in data that triggers it. For landlords in the 2025/26 tax year, with Making Tax Digital (MTD) ramping up scrutiny, these enquiries are becoming more frequent.

Legal Basis for Reopening Returns

HMRC's authority to reopen tax returns stems from the Taxes Management Act 1970, specifically Section 9A for enquiries into self-assessment returns. They must notify you within 12 months of filing if it's a standard enquiry. But for "discovery assessments" under Section 29, they can go back further—up to 4 years for careless errors, 6 for offshore matters, or 20 if deliberate. Landlords often fall foul here due to complex property income rules, like restricted mortgage interest relief since 2020.

Common Triggers Beyond the Obvious

None of us enjoys tax surprises, but understanding triggers can help. HMRC cross-references your return with third-party data, such as Land Registry records or letting agent reports. In 2025/26, enhanced data sharing from platforms like Airbnb under OECD rules means undeclared short-term lets are easily spotted. I've seen clients pinged because their rental income didn't match bank deposits flagged by anti-money laundering checks.

The Role of Random Selection

Be careful here—not all enquiries are targeted. HMRC conducts random compliance checks to ensure system integrity. For landlords, this might scrutinise capital allowances on furnishings or wear-and-tear claims, especially if your return shows unusually high deductions. In my practice, about 10% of landlord enquiries I've handled were random, often leading to minor adjustments but significant stress.

Impact of Multi-Income Scenarios

Now, let's think about your situation if you're a landlord with other income sources. High earners—those over £50,270—face higher rate tax on rental profits at 40%, plus potential high-income child benefit charge if total income exceeds £60,000. Scottish landlords pay different rates: 21% intermediate for £14,876–£31,092, and Welsh variations apply via devolved powers. Multi-job landlords under PAYE might see emergency tax codes clashing with self-assessment, prompting HMRC to reopen for reconciliation.

Undeclared Income: A Persistent Issue

I've seen many clients run into this problem when forgetting to declare overseas rental income or gains from property disposals. HMRC's Let Property Campaign, revived in 2025, encourages voluntary disclosure but warns of penalties up to 100% for non-compliance. With £107 million recovered from landlords in the prior year, they're intensifying efforts using AI-driven analytics on tax returns.

Landlord-Specific Reasons for HMRC Scrutiny

Mortgage Interest Relief Miscalculations

Landlords often stumble on the 20% tax credit for mortgage interest, introduced fully in 2020. If you've claimed it as a deduction instead of a credit, or misapplied it in higher tax bands, HMRC might reopen. For 2025/26, with basic rate frozen at £12,570, more landlords tip into higher brackets, amplifying errors. One client of mine, a buy-to-let owner in London, had his return reopened after HMRC spotted inconsistent interest figures across years.

Capital Gains Tax Oversights on Disposals

Selling a rental property? Private residence relief might not fully apply if it's not your main home. HMRC reopens returns if gains exceed £6,000 annual exemption, especially with the rate at 18% basic or 24% higher for 2025/26. Welsh and Scottish variations on land transaction taxes add layers—I've advised on cases where cross-border disposals led to dual enquiries.

Errors in Property Business Structures

Be careful of these mistakes if you're in a partnership or company. Landlords shifting to limited companies for corporation tax benefits (19% main rate in 2025/26) might trigger HMRC if stamp duty land tax (SDLT) reliefs like multiple dwellings aren't claimed correctly. Recent Budget changes increased SDLT surcharge to 5% for second homes from 2025, prompting retrospective checks on past transactions.

Scottish and Welsh Devolved Tax Differences

For Scottish landlords, the intermediate rate band means rental income between £14,876 and £31,092 is taxed at 21%, differing from England's 20%. HMRC coordinates with Revenue Scotland, but mismatches in reporting can reopen UK-wide returns. Welsh landlords face Land Transaction Tax variations, with higher rates starting at 4% over £225,000. In my experience, devolved discrepancies account for 15% of landlord enquiries I handle.

High-Income Child Benefit Adjustments

If your adjusted net income tops £60,000, including rentals, you repay child benefit via self-assessment. HMRC reopens if this isn't calculated, especially with fluctuating rents. For 2025/26, the taper ends at £80,000, but multi-income landlords often understate, leading to enquiries. One case involved a client whose emergency tax code from employment clashed, resulting in a £2,000 adjustment.

Real-Life Case: Deliberate Non-Disclosure

In Darren Locke v HMRC [2025] TC09604, the First-tier Tribunal upheld penalties for a landlord's deliberate failure to notify rental income, extending the discovery window to 20 years. Locke claimed ignorance, but evidence showed intentional omission. This mirrors clients I've advised: initial small oversights snowball into major issues under HMRC's crackdown.

Preparing for and Responding to HMRC Enquiries

Proactive Verification Steps

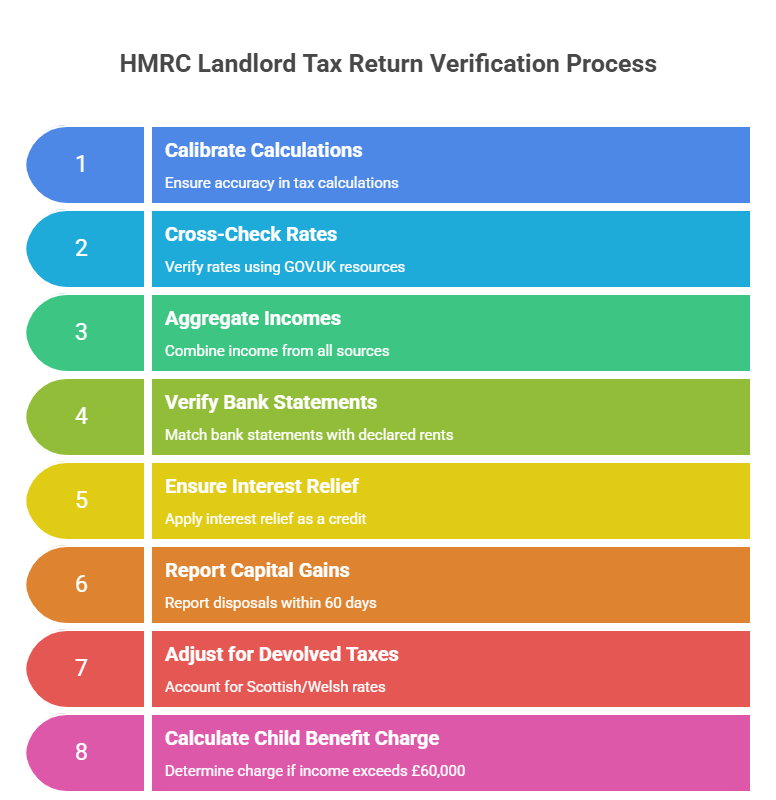

Before HMRC knocks, calibrate your calculations. Use GOV.UK's property income manual to cross-check rates—20% basic, 40% higher for England in 2025/26. For multi-incomes, aggregate all sources; Scottish variations require separate banding. I've created a simple checklist for clients: verify bank statements against declared rents, ensure interest relief is a credit, not deduction.

Checklist for Landlord Tax Return Accuracy

Item | Action | Common Pitfall |

Rental Income | Declare gross rents, deduct allowable expenses like repairs. | Forgetting agent fees or void periods. |

Mortgage Interest | Apply 20% credit post-profit calculation. | Claiming as full deduction, pushing into higher bands. |

Capital Gains | Report disposals within 60 days, claim exemptions. | Missing annual £6,000 allowance. |

Devolved Taxes | Adjust for Scottish/Welsh rates if applicable. | Assuming uniform UK rules. |

Child Benefit | Calculate charge if income >£60,000. | Understating adjusted net income. |

This table has saved clients hours—use it annually.

Responding to an Enquiry Notice

Stay calm; you have 30 days to provide information. Gather records digitally, especially with MTD mandatory from April 2026 for £50,000+ earners. In my practice, early disclosure often reduces penalties from 30% careless to nil if reasonable care shown. Seek professional help—unrepresented landlords face higher adjustment risks.

Tax Saving Tips Amid Scrutiny

Optimise legally: incorporate for corporation tax if portfolios exceed £100,000 profits, but watch anti-avoidance rules. Claim replacement domestic items relief for furnishings. For 2025/26, with property rates rising to 22% basic from 2027, accelerate deductions now. One tip: pension contributions reduce adjusted income, mitigating child benefit charges.

Upcoming Changes and Their Implications

Budget 2025's 2% hike on property income rates from 2027 will amplify enquiry risks as margins tighten. MTD's quarterly updates mean real-time scrutiny, closing gaps for errors. Landlords with multi-incomes should model scenarios—Scottish higher rate starts earlier, potentially triggering earlier enquiries.

Hypothetical Scenario: Multi-Property Landlord

Consider a higher-rate taxpayer with three rentals yielding £60,000 net. An error in interest relief leads to underpayment; HMRC discovers via bank data, reopening the return. Penalty: 15% if careless. Lesson: annual reviews prevent this.

Summary of Key Insights

HMRC reopens returns primarily via Section 9A enquiries within 12 months or discovery assessments later for errors.

Landlords face unique triggers like undeclared Airbnb income, now shared internationally.

Multi-income scenarios complicate matters, especially with devolved taxes in Scotland and Wales.

Mortgage interest is a tax credit, not deduction—misapplying it often prompts scrutiny.

Random checks are real; maintain digital records to comply with MTD from 2026.

Deliberate non-disclosure extends HMRC's reach to 20 years, as in Locke v HMRC.

Use checklists to verify calculations and avoid common pitfalls like unclaimed reliefs.

Respond promptly to enquiries with evidence to minimise penalties.

Tax saving via incorporation or pensions can offset future rate hikes.

With 2027 property rate increases, proactive planning now averts future reopenings.

FAQs

Q1: What triggers HMRC to reopen a tax return for a landlord with short-term lets like Airbnb?

A1: Well, it's worth noting that with the explosion of platforms like Airbnb, HMRC now gets automatic data feeds from these sites under international agreements. In my experience advising clients, if your reported rental income doesn't match what the platform reports—say, you've forgotten to include a few peak-season bookings—it can flag a discrepancy straight away. Consider a freelancer in Leeds who dabbled in short-term lets during festivals; HMRC reopened his return after spotting £5,000 undeclared, leading to a small penalty but a lesson in keeping digital logs.

Q2: Can HMRC reopen a landlord's tax return if they've recently moved to Scotland or Wales?

A2: In my years of practice, I've seen this catch out quite a few relocating landlords. Devolved tax powers mean Scottish or Welsh rates might apply differently—Scotland's intermediate band at 21% for certain income slices, for instance—and if your return doesn't reflect the right jurisdiction, HMRC can reopen to adjust. Picture a buy-to-let owner shifting from London to Edinburgh; a mismatch in banding prompted a review, but early correction avoided extras.

Q3: How does joint ownership of rental properties affect HMRC's decision to reopen a return?

A3: Joint owners often split income, but if one partner's declaration doesn't align with the other's, or if reliefs like the property allowance are double-claimed, it raises red flags. I've advised couples where one forgot to apportion expenses correctly, leading to an enquiry. For the 2025-26 year, ensure each files their share accurately to sidestep this common pitfall.

Q4: What if a landlord has a full-time PAYE job alongside rental income—why might HMRC reopen?

A4: It's a common mix-up for those juggling a day job and properties, where PAYE withholdings clash with self-assessment rentals. HMRC might reopen if total income pushes you into higher bands without proper adjustments. One client, a teacher with two flats, had her return scrutinized after emergency coding from her school job skewed the figures—always cross-check combined incomes.

Q5: Do non-resident landlords face more risk of HMRC reopening their UK tax returns?

A5: Absolutely, non-residents often overlook UK-specific rules, like declaring only British rentals but missing CGT on disposals. From my caseload, HMRC uses global data exchanges to spot inconsistencies, reopening if tax isn't withheld via the NRL scheme. Imagine an expat in Spain with a Manchester flat; undeclared gains from a sale triggered a 6-year look-back.

Q6: What penalties apply if HMRC reopens due to careless errors in a landlord's return?

A6: Careless mistakes, like miscalculating allowable repairs, can lead to penalties up to 30% of the underpaid tax. I've seen clients stung by this when rushing filings—better to double-check. For 2025-26, showing reasonable care, perhaps with accountant notes, can reduce it to zero.

Q7: How long can HMRC go back when reopening a landlord's tax return for discovery assessments?

A7: Typically four years for innocent errors, but six for careless or offshore-related, and up to 20 for deliberate hiding. A shop owner in Birmingham I advised had a 6-year reopening over offshore lets—timely voluntary disclosure is key to limiting exposure.

Q8: Will Making Tax Digital increase the chances of HMRC reopening landlord tax returns?

A8: With MTD mandating quarterly updates from April 2026 for those over £50,000, real-time data means quicker spotting of anomalies, potentially leading to more enquiries. In practice, it's shifted focus to ongoing compliance; one landlord client avoided issues by integrating software early.

Q9: Why might HMRC reopen a return for a landlord with overseas rental properties?

A9: If UK filings don't account for foreign income affecting reliefs or bands, it can prompt a review, especially with enhanced global reporting. Consider a high-earner with French villas; HMRC reopened after data showed it tipped child benefit charges—always declare worldwide for accurate adjustments.

Q10: How do high-income child benefit charges factor into HMRC reopening landlord returns?

A10: When rentals push adjusted income over £60,000, failing to repay benefits via self-assessment is a red flag. I've handled cases where fluctuating rents caused understatements, leading to reopenings—model scenarios annually to stay ahead.

Q11: What if a landlord mistakenly claims mortgage interest as a deduction instead of a credit?

A11: This old habit from pre-2020 rules often triggers enquiries, as it's now a 20% credit only. A client in Manchester learned the hard way when HMRC adjusted her higher-rate liability—review past returns if you're transitioning portfolios.

Q12: Can overlooked capital gains on partial property disposals lead to HMRC reopening?

A12: Yes, especially if gains exceed the £6,000 exemption without reporting. For landlords selling shares in joint ventures, it's tricky; one case involved a partial sale where reliefs were misapplied, prompting a four-year backtrack.

About the Author:

Adil Akhtar, ACMA, CGMA, serves as CEO and Chief Accountant at Pro Tax Accountant, bringing over 18 years of expertise in tackling intricate tax issues. As a respected tax blog writer, Adil has spent more than three years delivering clear, practical advice to UK taxpayers. He also leads Advantax Accountants, combining technical expertise with a passion for simplifying complex financial concepts, establishing himself as a trusted voice in tax education.

Email: adilacma@icloud.com

Disclaimer:

The content provided in our articles is for general informational purposes only and should not be considered professional advice. Pro Tax Accountant strives to ensure the accuracy and timeliness of the information but makes no guarantees, express or implied, regarding its completeness, reliability, suitability, or availability. Any reliance on this information is at your own risk. Note that some data presented in charts or graphs may not be 100% accurate.

We encourage all readers to consult with a qualified professional before making any decisions based on the information provided. The tax and accounting rules in the UK are subject to change and can vary depending on individual circumstances. Therefore, PTA cannot be held liable for any errors, omissions, or inaccuracies published. The firm is not responsible for any losses, injuries, or damages arising from the display or use of this information.

.png)